Internal Revenue Code Section 351

Section 351 Transaction U S Corporate Tax Youtube

How To Calculate Transferor S Basis Section 351 U S Corporate Tax Youtube

4 61 12 Foreign Investment In Real Property Tax Act Internal Revenue Service

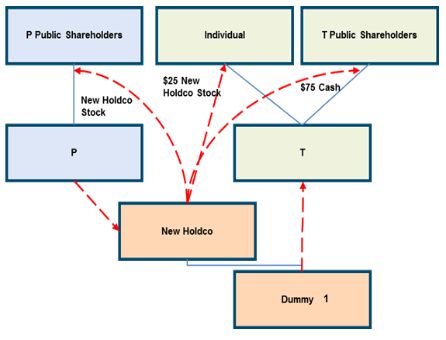

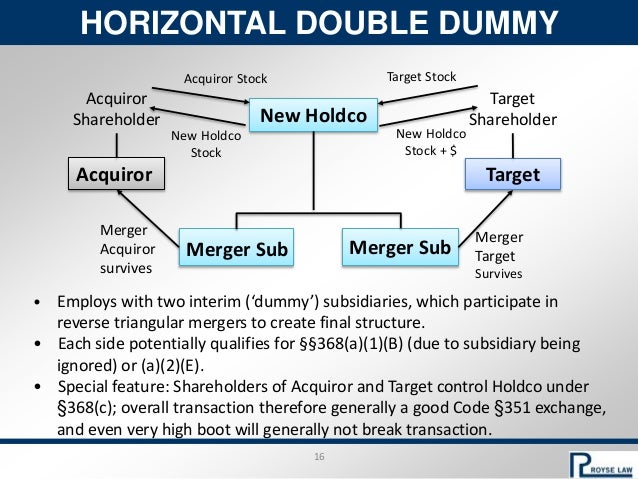

Achieving Tax Free Rollover Treatment For Certain Shareholders In Acquisition Of Publicly Traded Target Company Tax United States

Https Www Cigna Com Assets Docs About Cigna Form8937 Pdf

Startup Law A To Z Corporate Matters

Code unannotated title 26.

Internal revenue code section 351. 351 u s. Internal revenue code 351 findlaw. Corporate distributions and adjustments.

Section 351 a provides that no gain or loss will be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control as defined in 368 c of the corporation. Internal revenue code section 351. Internal revenue code 351.

Transfer to corporation controlled by transferor. Normal taxes and surtaxes. Transfer to corporation controlled by transferor.

Transfer to corporation controlled by transferor. No gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control as defined in section 368 c of the corporation. No gain or loss shall be recognized if property is transferred to a corporation by one or more persons solely in exchange for stock in such corporation and immediately after the exchange such person or persons are in control as defined in section 368 c of the corporation.

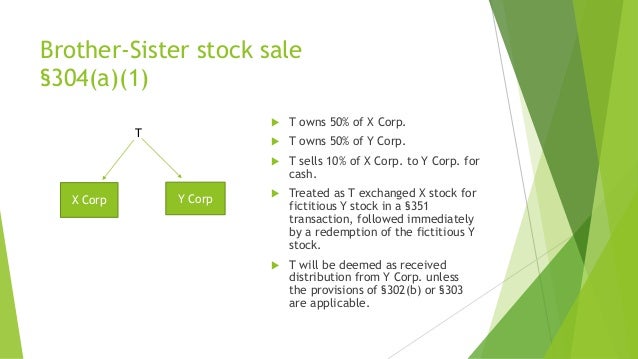

Code Sec 304 Related Party Stock Sales

Requirements For Nonrecognition Of Gain Or Loss On Transfer Of Property To A Corporation Irc 351 Taxconnections

M A Tax For 2019

Https Www Irs Gov Pub Int Practice Units Iso9411 08 01 Pdf

Boot And Relief Of Owner S Liabilities Henssler Financial

Https Taxworkbook Com Files 2016 09 Related Partiesweb Pdf

Lesson 3 5 1 Built In Loss Property Concepts Module 3 Corporate Formation I Coursera

Http Www Irs Gov Pub Int Practice Units Iso9411 08 03 Pdf

Https Www Law Uh Edu Faculty Bwells Ct2017 Chapter 202 Pdf

Https Tax Thomsonreuters Com Content Dam Ewp M Documents Tax En Pdf Brochures Checkpoint Catalyst Topics Brochure Pdf

Https Www Jstor Org Stable 20769172

Section 351 Transaction With The Transfer Of Services U S Corporate Tax Youtube

Https Www Jstor Org Stable 20767390