Delaware Franchise Tax Section

Faqs Delaware Corporation Annual Report And Franchise Tax Due Annual Report Report Delaware

Delaware Certificate Of Good Standing Delaware States Certificate

Delaware Certificate Of Dissolution Of Non Stock Corporation Section 276 A Download Fillable Pdf Templateroller

Delaware Foreign Llc Registration Get A Delaware Certificate Of Authority

Mitt Romney A Delaware Incorporator Incnow

Https Www Skadden Com Media Files Publications 2017 07 Delawarecodeamendmentsincreasefranchisetaxesforcor Pdf

Corporate tax refund returns 302.

Delaware franchise tax section. 302 739 3073 option 3 or click below. Taxes are assessed if the corporation is active in the records of the division of corporations anytime during january 1st through december 31st of the current tax year. Business license assistance 302 577 8778.

It is simply required by the state of delaware to maintain the good standing status of your company. Any delaware corporation that is ending its existence or reinstating their status to good standing is required by law to file an annual report and pay any and all tax due. The bank franchise tax is imposed on banking organizations.

Corporate franchise tax see division of corporations dosdoc ftax delaware gov. Please contact the franchise tax section at 302 739 3073 and select option 3 and option 1 or by email at dosdoc ftax delaware gov before submitting your renewal merger dissolution conversion or any other document filing that will end the existence or renew the status of your delaware corporation. Why incorporate in delaware.

The tax has no bearing on income or company activity. In the event of neglect refusal or failure on the part of any corporation to file a complete annual franchise tax report with the secretary of state on or before march 1 the corporation shall pay the sum of 200 to be recovered by adding that amount to the franchise tax as herein determined and fixed and such additional sum shall become a part of the franchise tax as so determined and fixed and shall be collected in the same manner and subject to the same penalties. Corporate tax auditors 302 577 8783.

More than one million business entities take advantage of delaware s complete package of incorporation services including modern and flexible corporate laws our highly respected judiciary and legal community a business friendly government and the customer service oriented staff of the division of corporations. The minimum tax is currently 175 00 using the authorized shares method and the minimum tax using the assumed par value capital method is 400 00 with a maximum tax of 200 000 00 for both methods unless it has been identified as a large corporate filer then their tax will be 250 000 00. Title 5 delaware code chapter 1 section 101 7 defines banking organizations.

You can also stay current on delaware corporate law. Franchise tax is the fee imposed by the state of delaware for the right or privilege to own a delaware company. The minimum tax is 175 00 for corporations using the authorized shares method and a minimum tax of 400 00 for corporations using the assumed par value capital method.

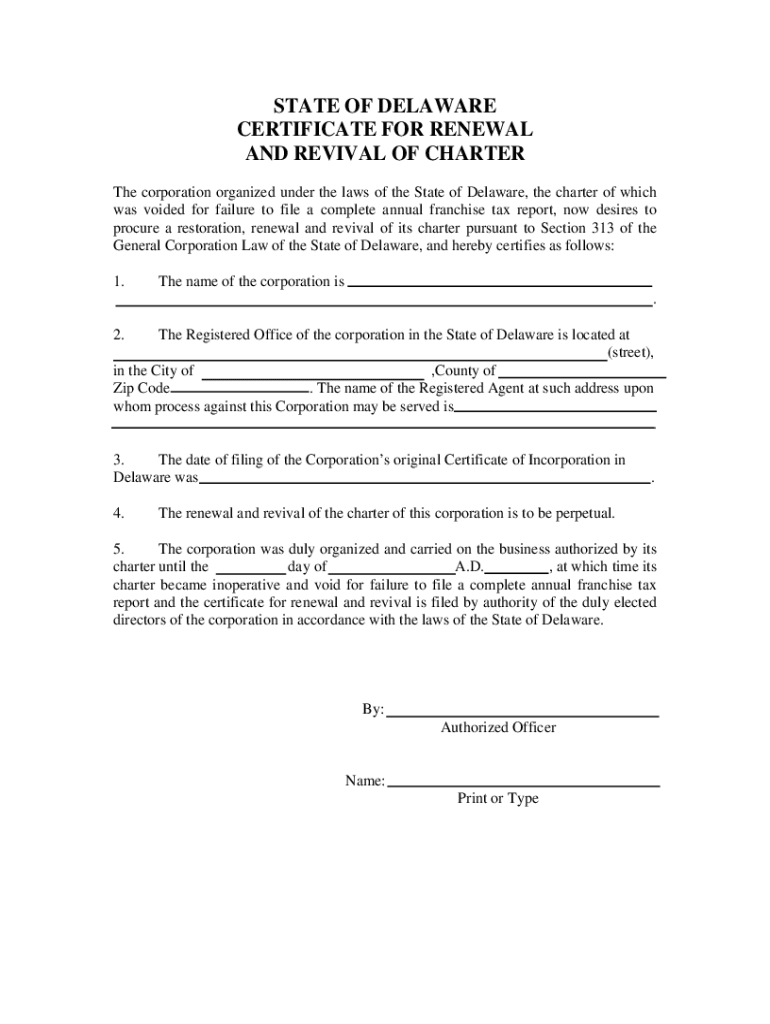

Https Corpfiles Delaware Gov Renewalvoid16 Pdf

Foundation Law Group Llp The Problematic Delaware Franchise Tax

Step 2 Requirements For Delaware Businesses Division Of Revenue State Of Delaware

Faqs About Delaware Franchise Tax

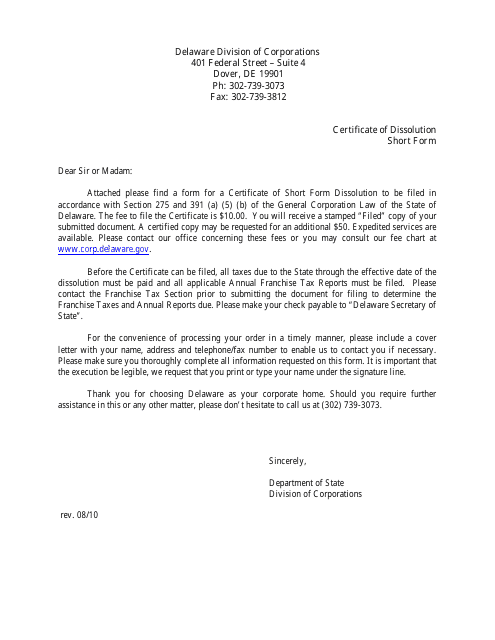

Certificate Of Dissolution State Of Delaware Division Of Corporations

Https Corpfiles Delaware Gov Dissolution 20 20274 20bis 20short 20form 20 20web Pdf

How To Register A Foreign Non Profit Corporation In Delaware

Delaware Certificate Of Dissolution For Non Stock Corporation Short Form Download Fillable Pdf Templateroller

State Of Delaware Certificate Of Cancellation Fill Out And Sign Printable Pdf Template Signnow

Will I Owe Taxes In The State Of Delaware Owe Taxes Delaware Tax

Https Delcode Delaware Gov Title8 Title8 Pdf

Pay Your Delaware Franchise Tax Registered Agent Fee Quickly And Easily Online With Harvard Business Services Inc I With Images Online Taxes Harvard Registered Agent

Delaware Short Form Certificate Of Dissolution Download Fillable Pdf Templateroller