Can You Take Section 179 On Leasehold Improvements

Section 179 Write Off Increases For 2018 Tax Deductions Deduction Writing

Section 179 And Bonus Depreciation In 2013 Blackburn Childers Steagall Cpas

Deduct Your Tattoo Removal Laser All About Section 179

Changes To Irs Section 179 What It Means For Facility Owners Air Force One

Section 179 Deduction A Guide For Creative Agencies

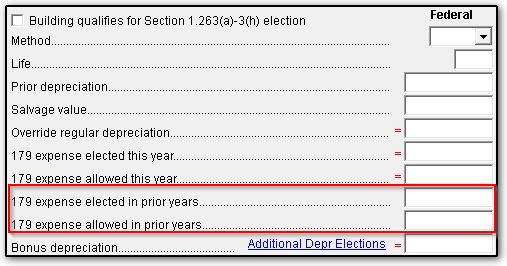

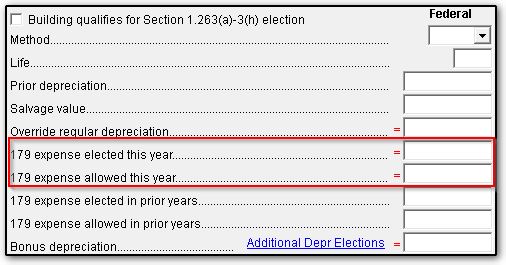

4562 Section 179 Data Entry

Section 179 historically was only applicable to tangible personal property not real property.

Can you take section 179 on leasehold improvements. Roofs heating ventilation and air conditioning property fire protection and alarm systems and security systems as long as the improvements are placed in service after the date the building was first placed in service. Qip qualified leasehold improvements qualified restaurant property and qualified retail improvement property may be eligible for section 179 expensing subject to certain limitations. The new roof will be capitalized on your depreciation schedule and expensed under section 179 provision and the old roof is removed.

In addition if these improvements meet the requirements to be qualified real property under irc section 179 and the other requirements of section 179 are met they may be eligible to be immediately expensed. You can elect the section 179 deduction instead of recovering the cost by taking depreciation deductions. Expensing under section 179 you can generally expense qualified leasehold improvements up to 500 000 adjusted annually for inflation under section 179 as opposed to depreciating them.

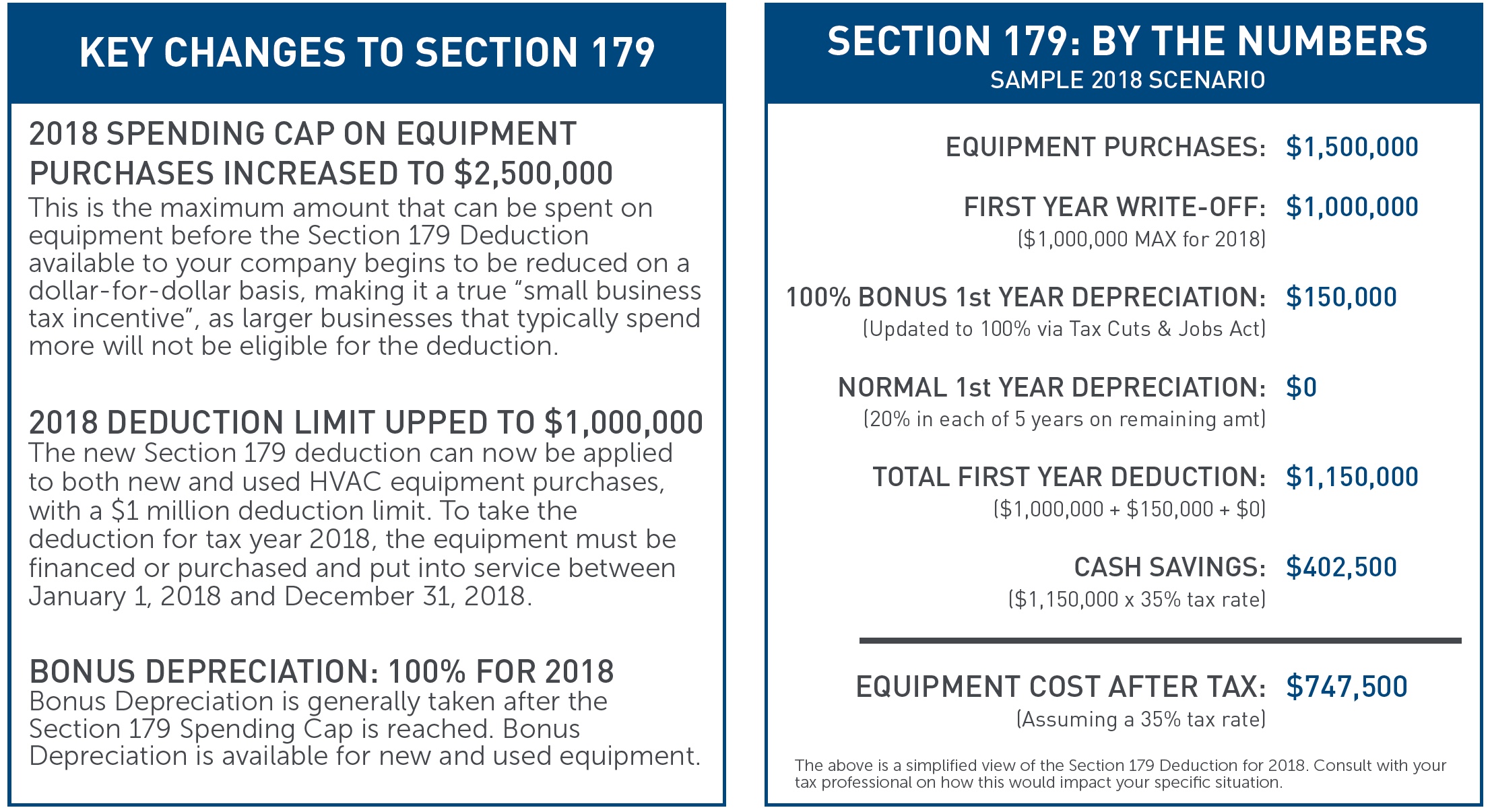

The new law increased the maximum deduction from 500 000 to 1 million. You can elect to recover all or part of the cost of certain qualifying property up to a limit by deducting it in the year you place the property in service. One of the major changes to section 179 expensing is the ability to fully deduct qualified leasehold improvements.

Improvement expenditures may be eligible for immediate expensing through section 179 depreciation. However section 179 begins to phase out when you place in service assets valued in excess of 2 000 000 in a single tax year. The rules for each category of qualified improvements have changed several times over the last decade making it difficult for tax professionals to keep track.

Qualified leasehold improvements can be expensed up to 250 000 for tax years beginning in 2010 and 2011. It also increased the phase out threshold from 2 million to 2 5 million. Once this is corrected lessees and building owners who improve qualifying business property will reap federal tax benefits of shorter depreciable lives increase bonus depreciation deductions and section 179 expensing.

What if you spent 750 000 on leasehold improvements this year for one of your retail strip plazas. This is the section 179 deduction. Who should make improvements landlord or tenant.

Irs Section 179 Deduction For 2017

Accounting For Assets Part 5 Insightfulaccountant Com

Deduction Is Section 179 Deduction Tax Deductions Writing

Section 179 Expense Election From Prior Year

1040 Us Section 179 Recapture Business Use 50

Section 179 Info On Section 179 And Deductions Depreciation More

Form 4562 A Simple Guide To The Irs Depreciation Form Bench Accounting

2018 Irs Section 179 Deduction News Update For Businesses

Irs Section 179 Asc 842 And Lease Vs Buy Decisions

Understanding Section 179 Tax Deduction For Small Business Infographic Small Business Infographic Tax Deductions Finance Infographic

Section 179 Deduction Irs Section 179 Deduction Limits For 2018 Were Raised To 1 000 000 With 100 Bonus Depreciation Up To 2 5 Deduction Irs Previous Year

Section 179 Irs Tax Deduction Updated For 2020

The Section 179 And Section 168 K Expensing Allowances Current Law And Economic Effects Everycrsreport Com