Section 1244 Stock Irs

Internal Revenue Bulletin 2017 26 Internal Revenue Service

Http Www Irs Gov Pub Irs Pdf P4491 Pdf

Fill Free Fillable Irs Pdf Forms

Freelance Taxes 3 50 Deductions You Ll Want To Take To Save Money Income Tax Deadline Income Tax Payroll Taxes

Irs Forms Publications Lattaharris Llp

Https Www Irs Gov Pub Irs Dft I8949 Dft Pdf

The corporation s equity may not exceed 1 000 000 at the time the stock is issued.

Section 1244 stock irs. However if the total loss is more than the maximum amount that can be treated as an ordinary loss for the year 50 000 or on a joint return 100 000 also report the transaction on form. The stock must be issued for money or property other than stock and securities. Section 1244 small business stock.

For starters 1244 benefits only apply to the original owners of the corporation. You can deduct as an ordinary loss rather than as a capital. Special rules may limit the amount of your ordinary loss if a you received section 1244 stock in exchange for property with a basis in excess of its fmv or b your stock basis increased because of contributions to capital or otherwise.

Section 1244 of the tax code allows losses from the sale of shares of small domestic. Qualifying as section 1244 stock. 1244 treatment unless the debt is evidenced by a security or arises out of the performance of personal services regs.

Additionally the stock must be common stock issued by a domestic corporation in exchange for cash or property not exceeding an initial value of 1 million. 1244 c 1 a at the time such stock is issued such corporation was a small business corporation. Small business section 1244 stock report an ordinary loss from the sale exchange or worthlessness of small business section 1244 stock on form 4797.

550 for more details including information on what is section 1244 small business stock. Where to claim a section 1244 loss. Individuals can claim losses of up to 50 000 and couples may claim up to 100 000.

Section 1244 stock refers to the tax treatment of restricted stock by the irs. In contrast capital losses are subject to an annual deduction limit of only 3 000. To qualify as section 1244 stock.

Pin On Letter Template

Http Www Irs Gov Pub Irs Prior I1040 1970 Pdf

What Is Section 1244 Stock For Small Business Windes

Small Business Stock Loss Deduction Sec 1244 Taxpm

Https Www Uaex Edu Business Communities Business Entrepreneurship Media 2017 20workbook 20vol 20b Pdf

Creative Touch Interiors Inc Sec Registration

The Value In Something Worthless Section 1244 Stock Hudson Oak Tax Advisory

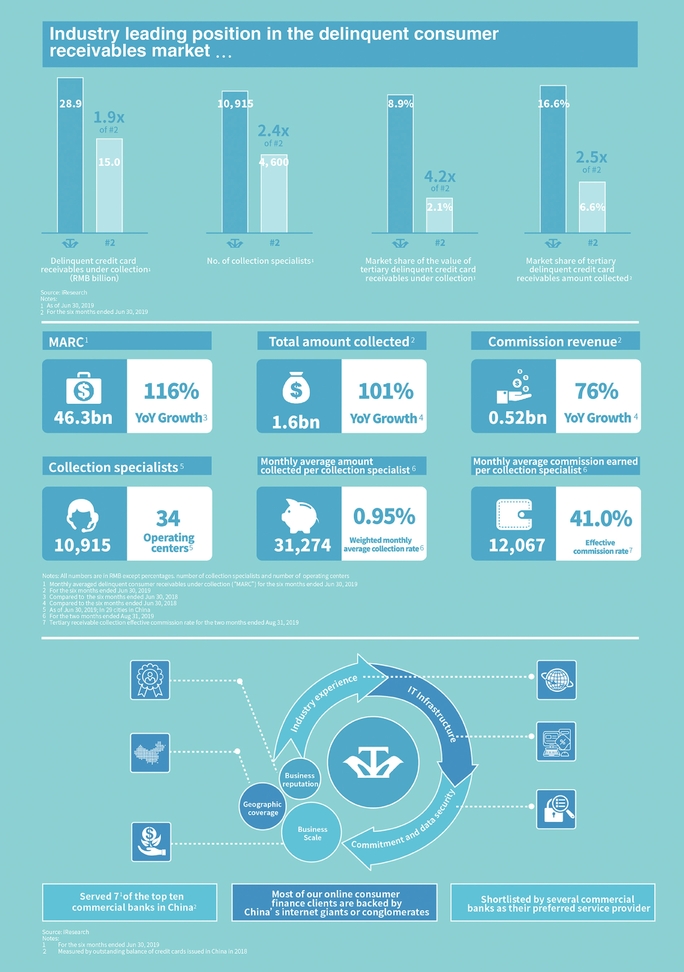

Yx Asset Recovery Limited

Pin By Som Sharma On Https Aroundtheindia Com Life Mood Motivation

Using Bankruptcy To Stop Foreclosure Bankruptcy Debt Relief Tax Debt Relief

Https Apps Irs Gov App Vita Content Globalmedia Teacher How To Complete Form 8949 4012 Pdf

Https Www Currentfederaltaxdevelopments Com S 201552026 Pdf

Pin On Talking Points