Section 105 Hra

Pin Na Nastence Dutinky

This Pie Chart Shows How Much Pie I Ate While Making This Chart Bizarrocomic Blogspot Com 2008 12 Time For Healing Social Media Humor Tech Humor Math Humor

Compare 2020 Hra Options With This Handy Tool From Core Documents Core Documents

New Restrictions On Employer Provided Medical Expense Reimbursement Plans Cliftonlarsonallen Cla Llp Medical How To Plan Employee Benefit

Core Documents Produces Video About Section 105 Hra Plan For 1 Employee Or Spouse Core Documents

Osiedle Kolorowy Goclaw Hra Architekci Architecture Residential Building Building Design

Section 105 plans are a type of reimbursement health plan that allows small businesses to reimburse their employees for medical costs tax free.

Section 105 hra. A section 105 plan is also tax free for the employee. Core documents specializes in the fsa and hra variations and the one person 105 hra form of section 105 of the code. Around since 1954 this type of hra was granted safe harbor in the affordable care act aca for businesses with 1 employee.

A section 105 plan is an irs regulated health benefit that allows the tax free reimbursement of medical and insurance expenses as described under section 105 of the internal revenue code irc. Section 105 of the internal revenue code was established to provide clear guidelines to small business owners and sole proprietors who purchase health insurance for themselves and their employees. As an employee enrolls in a qualified aca health plan they are then no longer subject to the tax penalty at the end of the year for not having health insurance.

They will advise the type of section 105 plan self insured qsehra stand alone reimbursement plans or group integrated hra plan to choose that best fits with the business legal structure. Section 105 plans are used by employers in a variety of ways. Section 105 plans play a huge role in the employer sponsored health insurance market particularly in self insured plans.

The base hra is an irs approved tax savings plan created through code section 105 of the internal revenue code that allows business owners the opportunity to deduct these expenses as a business deduction. Section 105 sets the following requirements for an eligible plan. Health reimbursement arrangements hras are a popular type of section 105 plan.

Moreover they are paying for part or all of their health plan premium from the reimbursable funds given to them by their employer. Next the business owner should choose a start date for the plan. Except as otherwise provided in this section amounts received by an employee through accident or health insurance for personal injuries or sickness shall be included in gross income to the extent such amounts 1 are attributable to contributions by the employer which were not includible in the gross income of the employee or 2 are paid by the employer.

Hra 105

Hra Plan Documents Hra Plan Designs Qualified Small Employer Hra

Matematika Oskola Specialni Pedagogika

Vysledek Obrazku Pro Basnicky Pro Maminku Inspiracni Citaty Maminka Basne

Hra

Video How To Save On Group Health Premium With An Hra Plan Documentcore Documents

Vilac Hrkajuce Kocky So Zvieratkami Kocky Hracky Deti

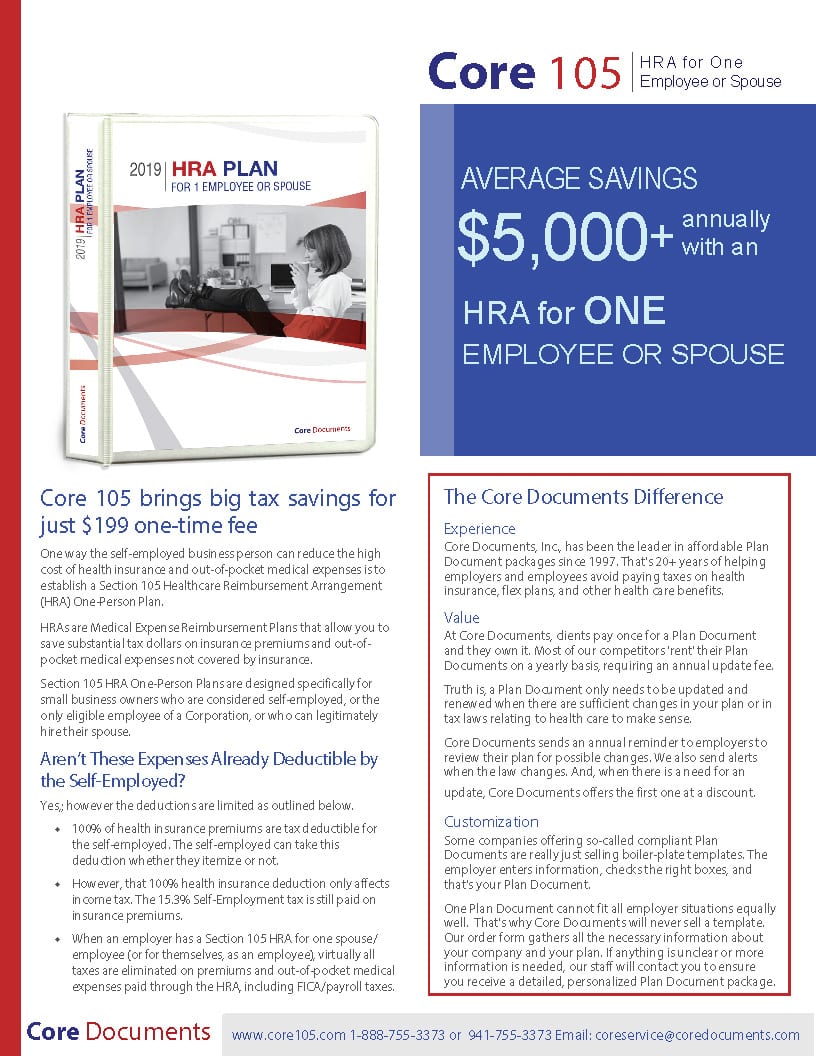

Core Section 105 Hra 1 Employee Hra Plan Document Forms Core Documents

Deductible Gap Hra Video How To Save On Group Health Premiums Core Documents

Church Employee Hra Provides Better Health Coverage Lower Cost With Video Core Documents

Vhodne Pro Deti Kabelove Svorky V Boxu Wago Wa 741 644 Pro Kabel O Rozmeru 0 14

How Employers Save Money With An Hra Real Life Example Core Documents