Internal Revenue Code Section 1445

Non Foreign Affidavit Under Irc 1445 Legal Forms Internal Revenue Code Real

3 21 261 Foreign Investment In Real Property Tax Act Firpta Internal Revenue Service

3 22 15 Foreign Partnership Withholding Internal Revenue Service

Https Www Illinois Ticortitle Com Services Non Foreign Certification Transferee 20transferor Pdf

3 21 15 Foreign Partnership Withholding Internal Revenue Service

Foreign Affidavit Pdf Fill Out And Sign Printable Pdf Template Signnow

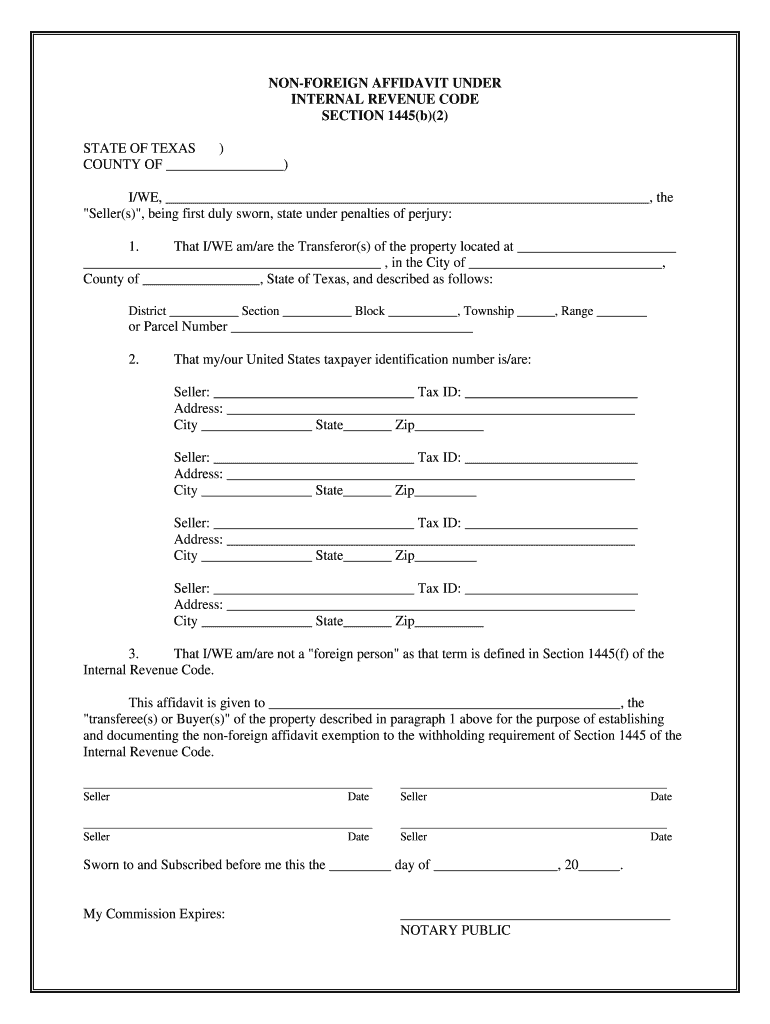

Certificate of non foreign status section 1445 of the internal revenue code provides that a transferee buyer of a u s.

Internal revenue code section 1445. Code 1445 withholding of tax on dispositions of united states real property interests. Section 1445 of the internal revenue code provides that a transferee buyer of a u s. Except as otherwise provided in this section in the case of any disposition of a united states real property interest as defined in section 897 c by a foreign person the transferee shall be required to deduct and withhold a tax equal to 15 percent of the amount realized on the disposition.

Real property interest must withhold tax if the transferor is a foreign person. Internal revenue code 1445. In general section 1445 a provides that any person who acquires a u s.

For additional information on the withholding rules that apply to partnerships refer to discussion under partnership withholding. Real property interest from a foreign person must withhold a tax of 15 percent 10 percent in the case of dispositions described in paragraph b 2 of this section from the amount realized by the transferor foreign person or a lesser amount established by agreement with the internal revenue service. Real property interest under local law will be the transferor of the property and not the disregarded entity.

Section 1445 of the internal revenue code provides that a transferee of a u s. For additional information on the withholding rules that apply to corporations trusts estates and reits refer to section 1445 of the internal revenue code and the related regulations. Real property interest must withhold tax if the transferor seller is a foreign person.

Tax purposes including section 1445 the owner of a disregarded entity which has legal title to a u s.

2 3 35 Command Code Irptr Internal Revenue Service

20 1 9 International Penalties Internal Revenue Service

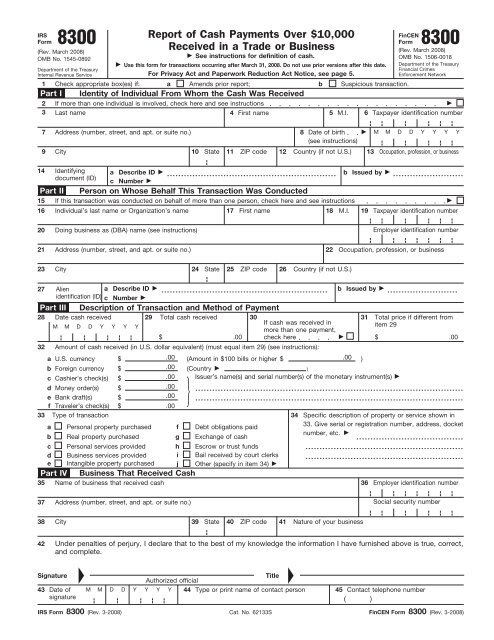

Irs Form 8300 Auction Com

3 21 3 Individual Income Tax Returns Internal Revenue Service

20 1 2 Failure To File Failure To Pay Penalties Internal Revenue Service

Firpta Form

4 61 12 Foreign Investment In Real Property Tax Act Internal Revenue Service

3 12 179 Individual Master File Imf Unpostable Resolution Internal Revenue Service

Certificate Of Non Foreign Status Free Download

3 11 6 Data Processing Dp Tax Adjustments Internal Revenue Service

W 8ben Form Irs Gov State Tax Teachers College

Https Www Wra Org Lu1911

Find Irs Form 990 Professional Advice At Charitynet Usa Tax Forms Irs Forms Internal Revenue Code