Code Section 754

Https Checkpointlearning Thomsonreuters Com Liveevent Download Location Prod Ecom H0191 Westlan Com Cpl Prod Marketing Webinarattachments 1369 12 29 16 20w238t Pdf Filename 12 29 16 20w238t Pdf

Partnership Taxation What You Should Know About Section 754 Elections

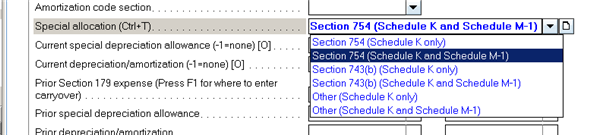

Entering Section 754 743 B Or Other Specially All Intuit Accountants Community

Section 754 Inside Basis Vs Outside Basis Taxation Of Partnerships

What S New In Ibm Developer For Z Os V14 2 3 Mainframe Dev

Https Www Bankofengland Co Uk Media Boe Files Prudential Regulation Regulatory Reporting Insurance Solvency Ii Xbrl Filing Manual Pdf

A section 754 election can be a favorable tax efficiency tool that is unique to partnerships as compared to corporations.

Code section 754. Section 754 of the us internal revenue code provides a set of rules that govern the tax allotted for a partner. Section 754 allows a partnership to make an election to step up the basis of the assets within a partnership when one of two events occurs. The purpose of a section 754 election is to reconcile a new partner s outside and inside basis in the partnership.

The basis of partnership property shall not be adjusted as the result of a transfer of an interest in a partnership by sale or exchange or on the death of a partner unless the election provided by section 754 relating to optional adjustment to basis of partnership property is in effect with respect to such partnership or unless the partnership has a substantial built in loss immediately after such transfer. A section 754 depreciation adjustment reported on the supplemental information page of a k 1 does not usually need to be reported anywhere on the individual tax return. Every general partner of a partnership should be aware of these rules and their implications.

Manner of electing optional adjustment to basis of partnership property. Eiseman a principal in cummings lockwood s private clients and corporate and finance group published an article entitled a review of code section 754 and its tax consequences which appeared in bloomberg bna tax management real estate journal vol. You can verify that the adjustment does not need to be entered by reviewing the supplemental information to see if the depreciation adjustment is reducing the net income.

This step up in basis is used to make the outside basis basis of the partnership in the hands of the owner equal to the inside basis the basis of the assets in partnership for tax purposes. However the complexity administrative burden and changing economic environment should always be considered carefully. Under section 754 a partnership may elect to adjust the basis of partnership property when property is distributed or when a partnership interest is transferred.

If a partnership files an election in accordance with regulations prescribed by the secretary the basis of partnership property shall be adjusted in the case of a distribution of property in the manner provided in section 734 and in the case of a transfer of a partnership interest in the manner provided in section 743. Section 754 requires each partner to determine their adjusted basis in order to determine the exact tax liability of the partner. To read a pdf of the article see below.

Machine Operator Resume Example In 2020 Resume Examples Resume Guide Resume

07 A Rose On Her Toes Ricamo Disegni

Primitive Data Types Language Types Java Tutorial Java Programming Language

Working With Authority Records Ex Libris Knowledge Center

Accounting Assistant Resume Sample In 2020 Resume Guide Software Engineer Accountant Resume

Ee017a782e0c2355c01fe2206090bc34 Jpg 564 754 Symboler Och Betydelse Initialer Tatueringsideer

Hotel Receptionist Resume Template In 2020 Guided Writing Receptionist Resume Guide

Au Pair Resume Sample In 2020 Civil Engineer Resume Resume Resume Examples

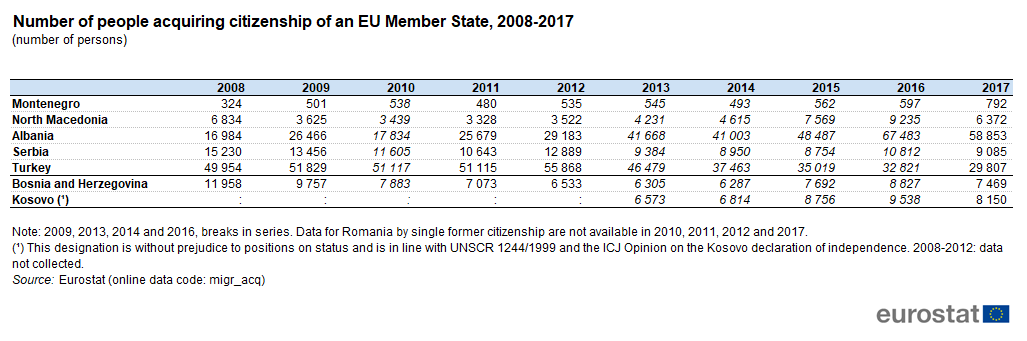

Enlargement Countries Statistics On Migration Residence Permits Citizenship And Asylum Statistics Explained

Staff Nurse Resume Template In 2020 Nursing Resume Nursing Resume Template Pediatric Nursing

Pin On Car Mechanic Resume Examples

Enlargement Countries Energy Statistics Statistics Explained

Frequency Of Qr Code Usage Among German Millennials 2017 Statista