Section 9 1 E Of The Income Tax Act

Income Tax Intimation Efiler Income Tax Intimation U S 143 1 Demand Notice 139 9 Service Income Tax Act Income Tax Income Tax Income Tax Return Income

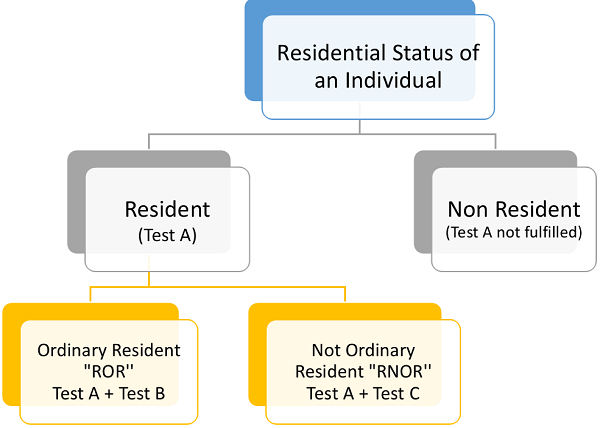

Learn The Basic Qualifications For Residency Status In Pakistan Online Taxes Filing Taxes File Taxes Online

Learn How You Can Claim Tax Credit For Investments In Shares For Savings Online Taxes Filing Taxes Tax Credits

Residential Status Under Income Tax Act 1961 Revisited

How To Check If Aadhaarcard Is Linked With Pancard Income Tax Return Income Tax Tax Return

Income Tax Slab Rates In India For A Y 2019 20 F Y 2018 19 For Individual Income Tax Income Tax

Income 9 1 subject to this part a taxpayer s income for a taxation year from a business or property is the taxpayer s profit from that business or property for the year.

Section 9 1 e of the income tax act. Indian income tax laws cover residents non residents and residential but non ordinary residents taxpayers within its ambit of tax liability. The income tax department appeals to taxpayers not to respond to such e mails and not to share information relating to their credit card bank and other financial accounts. Section 9 of income tax act income deemed to accrue or arise in india.

I all income accruing or arising whether directly or indirectly through or from any business connection in india or through or from any property in india or through or from any asset or source of income in india 4 or through the transfer of a capital asset situate in india. I all income accruing or arising whether directly or indirectly through or from any business connection in india or through or from any property in india or through or from any asset or source of income in india or through the transfer of a capital asset situate in india. 1 the following incomes shall be deemed to accrue or arise in india.

It might nevertheless be possible to transfer the residence to the beneficiary free of transfer duty under section 9 4 b of the transfer duty act. 30 i all income accruing or arising whether directly or indirectly through or from any business connection in india or through or from any property in india or through or from any asset or source of income in india or through the transfer of a capital asset situate in india. The latter provision applies when the beneficiary taking transfer is a relative of the trust s founder and does not pay any consideration e g.

Act specifies that for the income to be taxed in india it should deemed to accrue or arise in india. Section 9 1 of the i t. Income deemed to accrue or arise in india.

As per section 9 of the income tax act 1961 certain incomes are considered to have been earned in india even if they accrue or arise outside india. Section 9 1 in the income tax act 1995. 1 the following incomes shall be deemed to accrue or arise in india.

The act also imposes a tax liability on the income of the foreign companies and non resident indians to the extent such income is sourced within india. No income of a non resident can be taxed in india unless it falls within the four corners of section 5 read with section 9 of the income tax act. Rent for the residence whether directly or.

What To Do If My Employer Does Not Pay Tds Tax Deducted At Source Employment Income Tax

Reset Password Income Tax Income Tax Return File Income Tax

Health Insurance Provides You With A Security For You And Your Family During Medical Emergencies Acc Health Insurance Policies Income Tax Buy Health Insurance

Tax And Law Directory Gst Problems And Solutions Related To Banking I Problem And Solution Stock Broker Banking

Best Option To Save Tax For Salaried Mudra Home Best Option To Save Tax For Salaried Mudra Home Compare Apply Best Bank Loan Lowest Interest Rate In

File An Extension Pay On Time A Key Tax Reminder From Your Cpa Firm Filing Taxes Cpa Bookkeeping Services

Section 80ccc Deduction For Contribution Towards Pension Funds Pension Fund Tax Deductions Pensions

Variance Analysis Formula Need Importance Limitations Types Variance Ana In 2020 Financial Accounting Accounting And Finance Business Finance

Complete Schedule Income Taxes Stock Photo Sponsored Income Schedule Complete Photo Ad Income Tax Income Tax Forms

Tax Saving Benefits On Home Loan 2 Income Tax Act Section 80c Allows Home Buyers To Get A Maximum T Portfolio Management Home Loans Real Estate Investing

E File Itr Itr Amp Tax Filing Online Very Simpale With Allindiaitr How To Filing Itr Income Tax Return 31st Mar Income Tax Return Tax Return Income Tax

4 Tax Tips For Small Business Owners Tips Taxes Taxtime Income Tax Tips Tax Return Tips Small Business Tax Business Tax Small Business

Form 15g 15h What Is Form 15g How To Fill Form 15g For Pf Withdrawal