Section 78 Of Income Tax Act

Filing A Federal Tax Extension Cnbc Explains Tax Extension Federal Taxes Income Tax

3 Tax Deductions That Could Lead To An Audit Prove Torcoes

Section 87a Tax Rebate Fy 2019 20 How To Check If You Are Eligible For The Tax Rebate How To Check If You Are Eligible To Claim Sect Wealth Tax Rebates Tax

Pin On Stuff That Might Interest You

Save Tax Up To Rs 45 000 Invest In Mutual Fund Elss Advantages Of Mutualfund Elss Schemes Over Other Tax Saving In Finance Saving Investing Mutuals Funds

Pin By Bluefish Emarketing Mauritius On Business Economy Tax Services Budgeting Finances Service Advisor

1 where a change has occurred in the constitution of a firm nothing in this chapter shall entitle the firm to have carried forward and set off so much of the loss proportionate to the share of a retired or deceased partner as exceeds his share of profits if any in the firm in respect of the previous year.

Section 78 of income tax act. Income tax assessment act 1936 sect 78acertain gifts not to be allowable deductions. This act may be cited as the income tax act. Note on maternity leave pay tax deduction section 11 of the maternity protection act ch.

Certain gifts not to be allowable deductions. 254 and shall be ascertained in the same manner as annual value is ascertained under that act. Section 78 motor vehicle fringe benefit section 79 private expenditure fringe benefit section 80 property fringe benefit.

1 in this act unless the subject or context otherwise requires. B payment by promissory note. Index table search search this act notes noteup previous next download help income tax assessment act 1936 sect 78a.

Application of the act. Agreement includes any agreement arrangement or understanding whetherformal or informal or express or implied and whether or not enforceable bylegal proceedings. Deferring tax under part xiii of the act where the creditor is a non resident.

This act applies to years of income commencing on or after 1st july 1997. 1 in this section. 1 short title 2 part i income tax 2 division a liability for tax 3 division b computation of income 3 basic rules 5 subdivision a income or loss from an office or employment 5 basic rules 6 inclusions 8 deductions 9 subdivision b income or loss from a business or property 9 basic rules 12 inclusions.

Section 78 of income tax act 1961 2017 provides for carry forward and set off of losses in case of change in constitution of firm or on succession. Income tax act 2015 no 32 of 2015 1 commenced on 1 january 2016 except section 9 and part 6 which commence on the date notified by minister in the gazette as amended by. The income tax act.

Income Tax Form Medical Expenses The Ultimate Revelation Of Income Tax Form Medical Expenses In 2020 Tax Forms Income Tax Income

Https Moj Gov Jm Sites Default Files Laws The 20income 20tax 20act 0 Pdf

The Inland Revenue Is Responsible To The Government For The Administration Of The Income Tax And Capital Transfer Duty Acts And Income Tax Finance No Response

Calculation Of Foreign Tax Credit In Canada Depends Upon Source Of Foreign Income Tax Credits Tax Financial Statement

3 11 3 Individual Income Tax Returns Internal Revenue Service

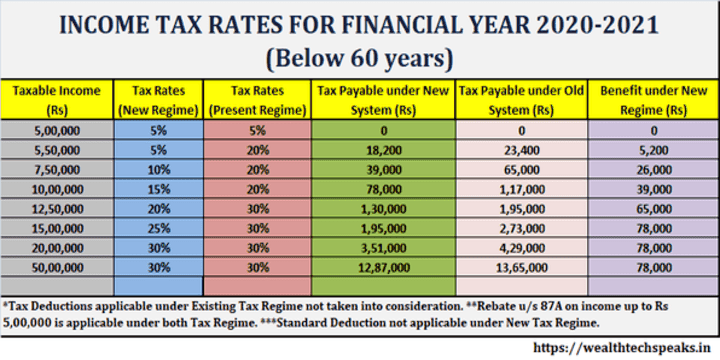

Income Tax Financial Year 2020 2021 Ay 2021 22 Tax Implications Wealthtech Speaks

Income Tax Dues Are Operational Debts Under Ibc Income Tax

Pdf National Budget 2019 20 Income Tax And Amendments In The Income Tax Laws An Overview

How To File 12a And 80g Registration Online Corpbiz Advisors The Power Of Collaboration In 2020 Income Tax Family Trust Income Tax Return

Due Date To File Income Tax Return Ay 2016 17 Fy 2015 16 Simple Tax India Income Tax Return Tax Return Income Tax

Organize Small Business Taxes Plus Free Printables Small Business Tax Business Organization Business Tips

Only One In Five Landlords Expected To Pay More Tax Under Section 24 Being A Landlord Income Tax Money Matters

Pin On Law Tax Business