Section 318 Attribution Rules

1 318 2 A Ex 2 Section 318 Attribution Youtube

Stock Ownership Using Section 318 Stock Attribution Rules P6 43 Youtube

Compound Interest The Chemistry Of Poisonous Frogs And How They Avoid Poisoning Themselves Chemistry Study Chemistry Organic Chemistry

Charts Of Examples In Code 6038a Regulations Form 5472 Reporting Requirements International Tax Blog

318 Upstream Trust Attribution In 2020 Tax Lawyer Tax Attorney

Ppt Stock Redemptions Powerpoint Presentation Free Download Id 5759693

Struck out sidewise attribution by providing that when stock is attributed to a partnership estate trust or corporation.

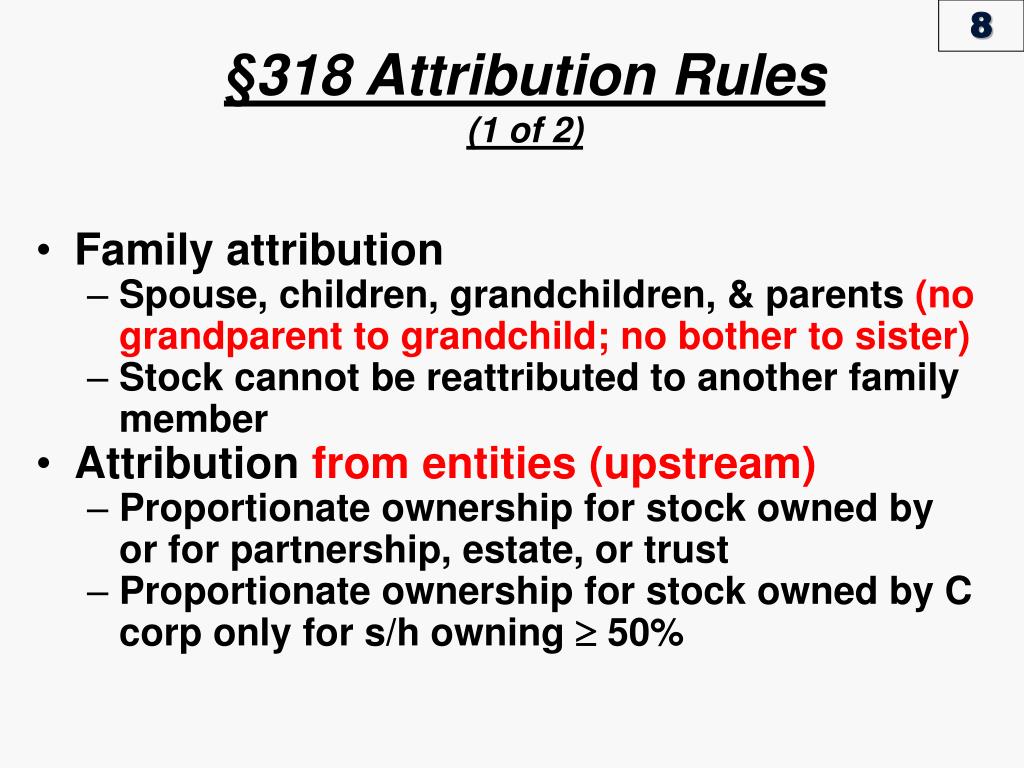

Section 318 attribution rules. For purposes of those provisions of this subchapter to which the rules contained in this section are expressly made applicable 1 members of family. General rule for purposes of those provisions of this subchapter to which the rules contained in this section are expressly made. While straightforward waiving family attribution is subject to several restrictions including the stringent separation requirements discussed below.

If patricia owns 50 of the business and. For purposes of these 35 percent ownership rules an individual will be treated as a constructive owner only if that individual himself or herself is a substantial contributor a foundation manager or a 20 percent owner of the combined voting power profits interest or beneficial interest of a substantial contributor. Attribution to partnerships estates trusts and.

For example if f and his two sons a and b each own one third of the stock of a corporation under section 318 a 1 a is treated as owning constructively the stock owned by his father but is not treated as owning the stock owned by b. Code 318. Section 318 a 5 b prevents the attribution of the stock of one brother through the father to the other.

Waiving family attribution is the exception to the general rule provided under section 318 a that instructs that a parent will be considered to own any stock owned by his or her children. An individual shall be considered as owning the stock owned directly or. Attribution rules mark out the legal principal owners of a firm and are in place to prevent tax evasion or fraud.

Constructive ownership of stock. Internal revenue code section 318 a 1. Under the section 1563 rules however attribution does not apply if all four of the following conditions are satisfied.

Attribution from partnerships estates trusts and corporations a from partnerships and estates. For adult children and grandchildren the attribution applies only to individuals who own more than 50 of the business. For purposes of those provisions of this subchapter to which the rules contained in this section are expressly made applicable 1 members of family.

Instructions For Form 5471 02 2020 Internal Revenue Service

An Example Of Work Package Instances Regrouping By Quotas 318 Download Scientific Diagram

Gale Onefile Health And Medicine Document Integrated Care Programs For People With Multimorbidity In European Countries Ehealth Adoption In Health Systems

Stock Redemptions Tx Ppt Download

Pdf Clinical Guidelines Developing Guidelines

Super Trapp Quiet Mufflers Parts Muffler Quiet Small Engine

Gale Academic Onefile Document Testing Tarnishment In Trademark And Copyright Law The Effect Of Pornographic Versions Of Protected Marks And Works

Http Scholarship Law Wm Edu Cgi Viewcontent Cgi Article 2537 Context Facpubs

International Tax Compliance Ppt Video Online Download

Tax Reporting For Cross Border Transactions Froms Penalties Statu

Streamlined Domestic Offshore Procedures Center Http Bit Ly 2xcmuex Tax Lawyer Tax Attorney Business Tax

1 Million Stunning Free Images To Use Anywhere Dieselengines Me In 2020 Tenses English Teaching English Grammar English Grammar

Tiffany Carlson Gen 499 Final Paper Docxgender Equalitygender Equalitytiffany Carlsongen 499 General Education Capstonepatricia In 2020 Late Homework Tiffany Finals