Section 179 Depreciation Recapture

Understanding Depreciation Recapture When You Sell A Rental Property In 2020 Estate Tax Rental Property Capital Gains Tax

Income Tax Considerations When Transferring Depreciable Farm Assets Ag Decision Maker

1040 Us Section 179 Recapture Business Use 50

Tax Reform And Bonus Depreciation Block Advisors Block Advisors

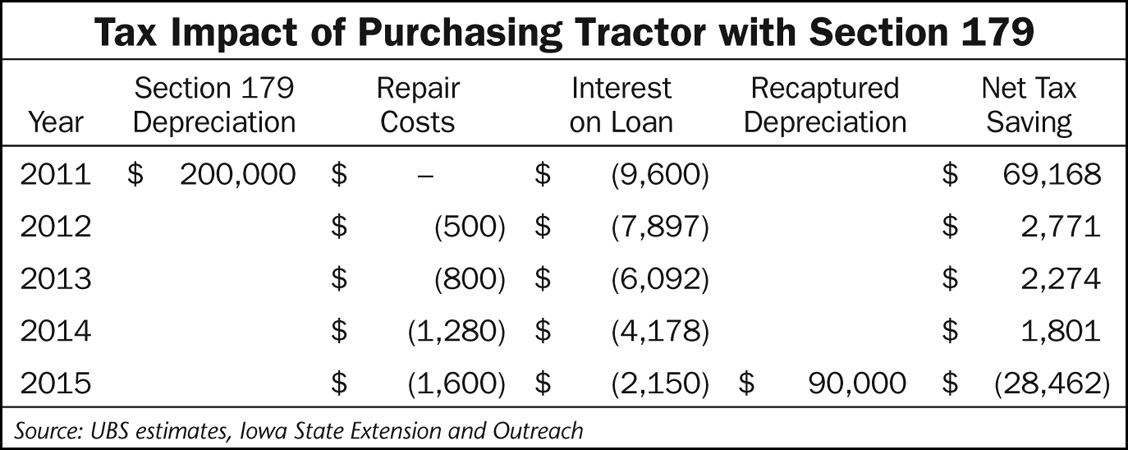

2013 Caution On Using Section 179 Depreciation

1040 Recapturing Depreciation

1245 to the extent of any gain realized on the disposition at the owner level.

Section 179 depreciation recapture. You can depreciate tangible property but not land. Alternatively you can depreciate the acquisition cost over a 5 year recovery period in the year you place the computer in service if you don t elect to expense any of the cost under section 179 the computer isn t eligible for the 100 special depreciation allowance in the year you place the computer in service or you decide to elect out of any special depreciation allowance for the class of property that includes computers. Since that s less than.

Return of partnership income if a passthrough entity disposed of sec. Figure the depreciation that would have been allowable on the section 179 deduction you claimed. Figure the depreciation that would have been allowable on the section 179 deduction you claimed.

To figure the amount to recapture take the following steps. Depreciation recapture applies to the lesser of the gain or your depreciation deductions. Tax depreciation section 179 deduction and macrs depreciation is the amount you can deduct annually to recover the cost or other basis of business property.

Income tax return for an s corporation or form 1065 u s. This must be for property with a useful life of more than one year. 179 property during the tax year the amount of the sec.

If you took a section 179 deduction for depreciation you must recapture depreciation in any year during the property s recovery period where your business usage of the asset drops below 50 percent. Subtract the depreciation figured in 1 from the section 179 deduction you claimed. Subtract the depreciation figured in 1 from the section 179 deduction you claimed.

The difference between the section 179 deduction and the used up portion of macrs depreciation is called a section 179 recapture and must be reported as income. 179 expense previously passed through to its owners on a schedule k 1 is treated as depreciation and must be recaptured under sec. Begin with the year you placed the property in service and include the year of recapture.

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

1040 Recapturing Depreciation

Ppt Ch 17

Economic Stimulus Implications

Section 179 Info On Section 179 And Deductions Depreciation More

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Farm Equipment

Section 1245 Depreciation Recapture Income Tax Course Cpa Exam Regulation Tax Cuts And Jobs Act Youtube

Section 179 Archives Custom Truck One Source

Section 179 Deduction Bonus Depreciation Depreciation Recapture Markets Wlj Net

Https Www Agmanager Info Sites Default Files Pdf Tax 20implications 20of 20farm 20financial 20planning 20decisions Klh Oct2017 Pdf

Advantages Disadvantages Of Accelerated Depreciation Small Business Chron Com