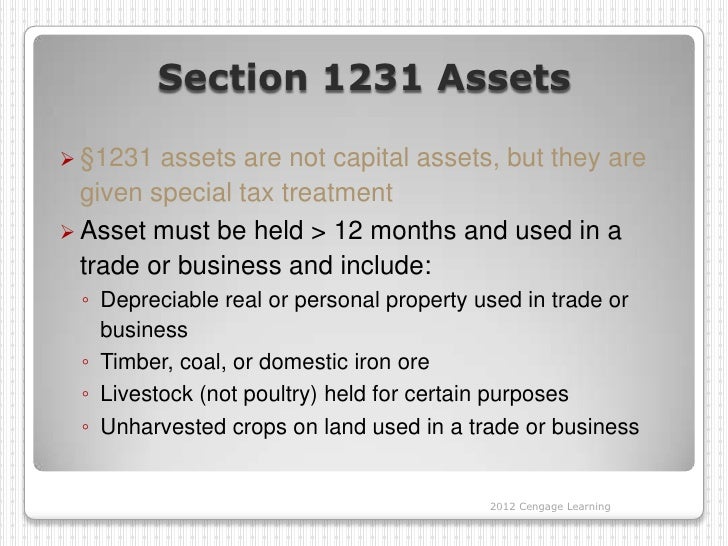

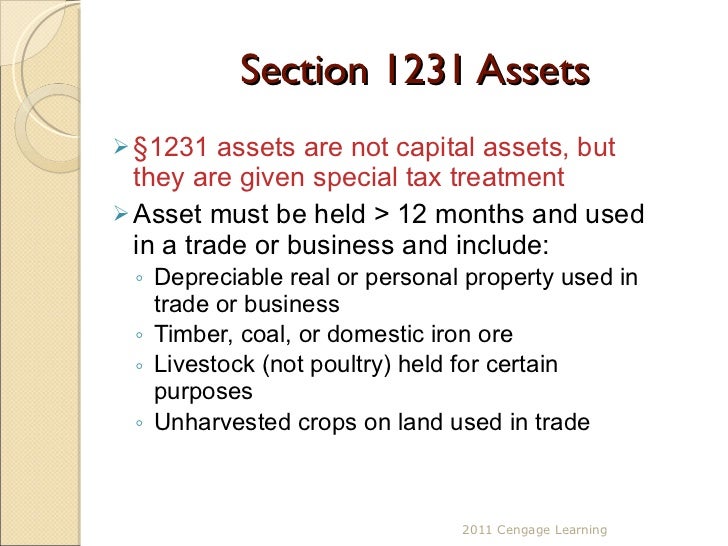

Section 1231 Assets Definition

Section 1231 Property

What Is 1231 Property What Does 1231 Property Mean 1231 Property Meaning Explanation Youtube

Ppt Ch 17

Taxation Of Business Entities Ppt Download

Chapter 13 Property Transactions Section 1231 And Recapture Ppt Download

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

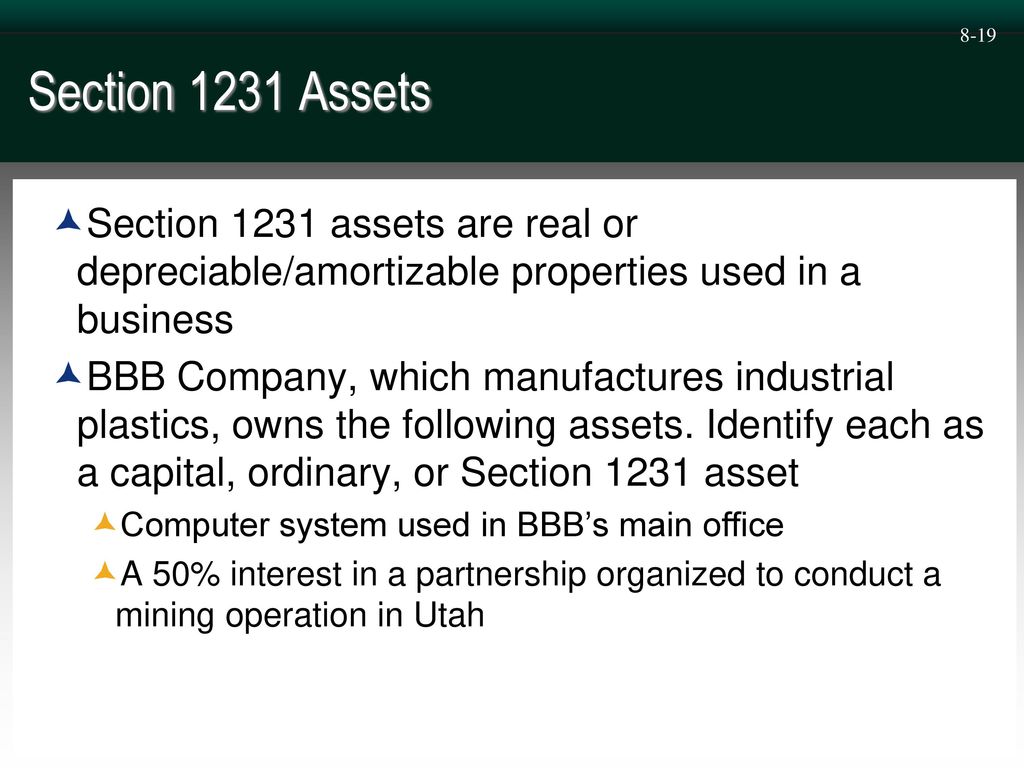

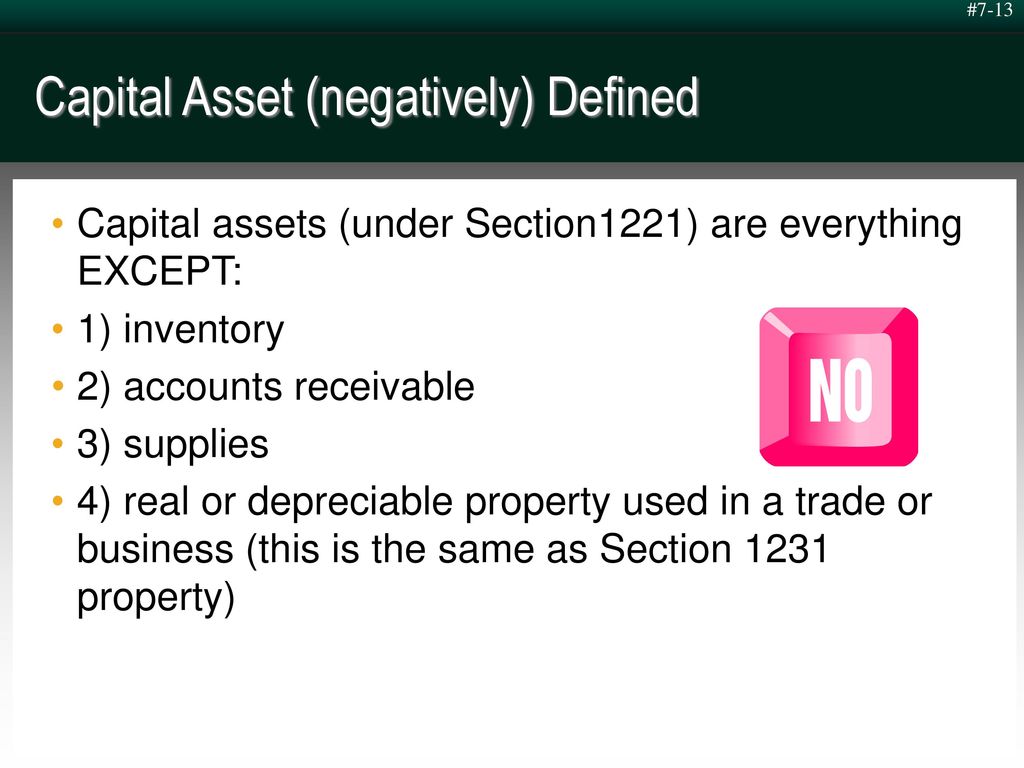

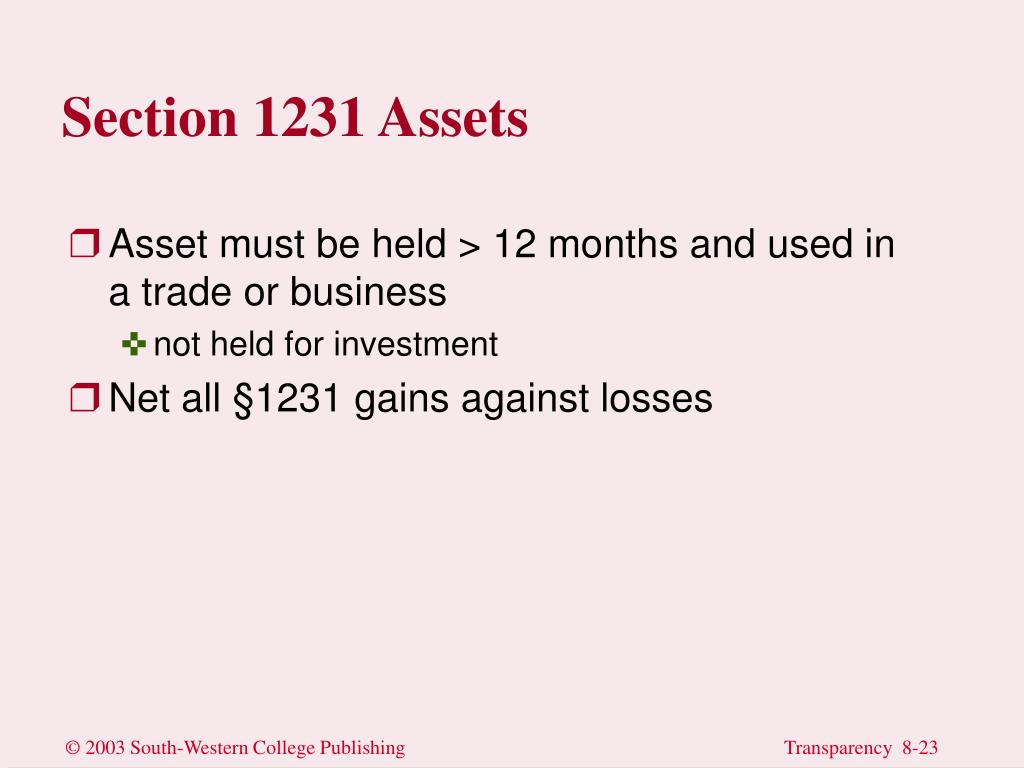

Buildings and equipment used in a trade or business and held for more than one year.

Section 1231 assets definition. Section 1231 property is real or depreciable business property held for more than one year. This property must be used in a trade or business and held longer than 1 year. Some types of livestock coal timber and domestic iron ore are also included.

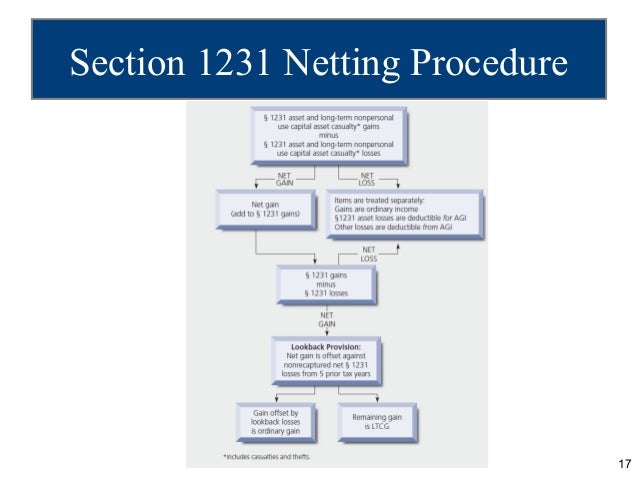

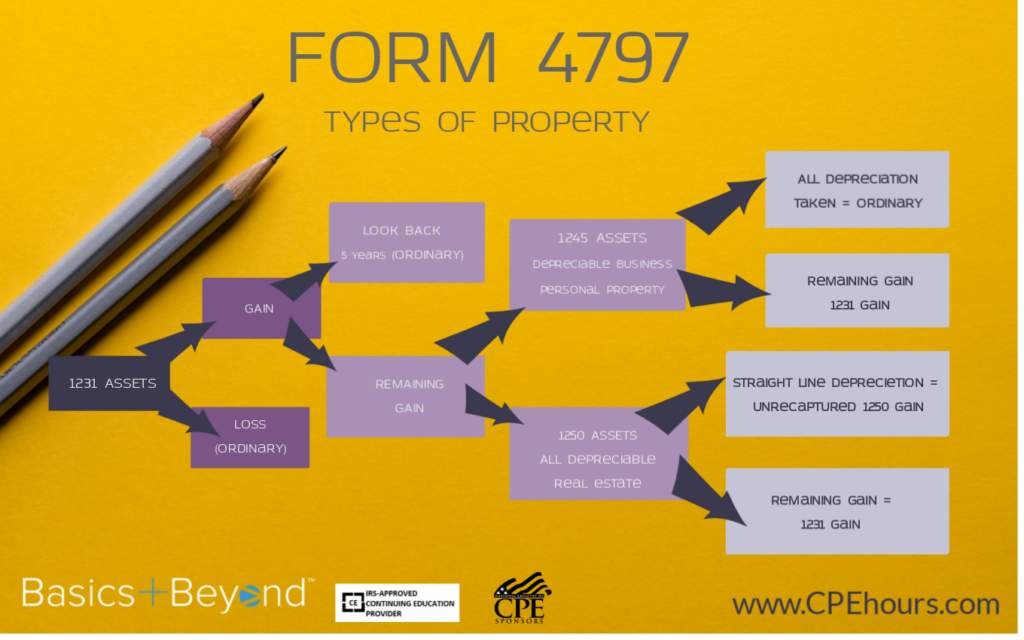

2 non recaptured net section 1231 losses for purposes of this subsection the term non recaptured net section 1231 losses means the excess of. Learn about 1231 1245 1250 property and its treatment for gains and losses. The net section 1231 gain for any taxable year shall be treated as ordinary income to the extent such gain does not exceed the non recaptured net section 1231 losses.

Is used for trade or business. Has been held for at least one year. Gain or loss on the business or rental part of the property may be a capital gain or loss or an ordinary gain or loss as discussed in chapter 3 under section 1231 gains and losses.

Section 1231 property is a type of property defined by section 1231 of the u s. Generally property held for the production of rents or royalties is considered to be used in a trade or business. Property used in a trade or business the internal revenue code includes multiple classifications for property.

1231 property is a category of property defined in section 1231 of the u s. 1231 property includes depreciable property and real property e g. Section 1231 property includes depreciable assets and real estate used in a trade or business and held for more than one year.

Under certain circumstances it also includes timber coal domestic iron ore livestock held for draft breeding dairy or sporting purposes and unharvested crops. You cannot deduct a loss on the personal part.

1231 1245 And 1250 Property Used In A Trade Or Business Investing Infographic Investment Quotes Investing

1231 1245 And 1250 Property Used In A Trade Or Business

Part 1 Introduction To 1231 Assets Coursera

Chapter 11 Property Dispositions Howard Godfrey Ph D Ppt Video Online Download

Chapter 8

Property Dispositions Ppt Download

Section 1231 Assets Income Tax Course Tax Cuts And Jobs Act Cpa Exam Regulation Tcja 2017 Youtube

Property Dispositions Ppt Download

Chapter 8 Capital Gains And Losses Ppt Download

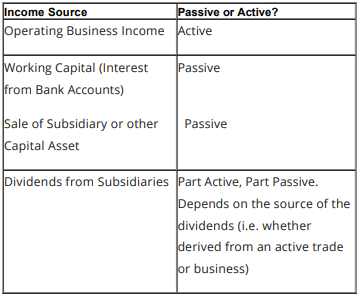

Pfic What U S Investment Funds Should Be Particularly Aware Of And Newly Proposed Regulations Lexology

Itf Ipp Ch08 2012 Final

Ppt Chapter 8 Powerpoint Presentation Free Download Id 1731275