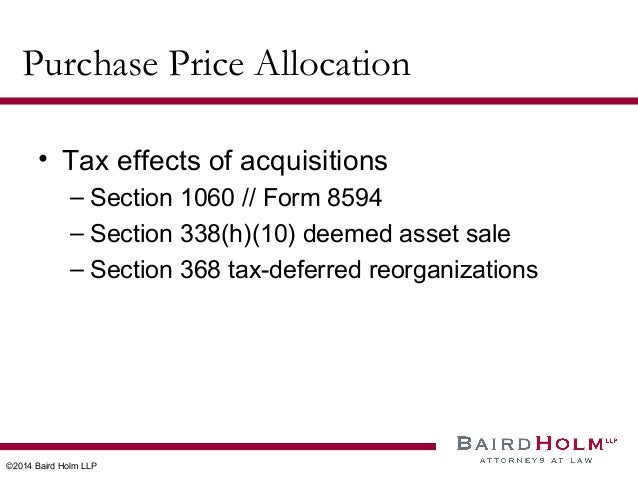

Section 1060 Purchase Price Allocation

Purchase Price Allocation Redwood Valuation

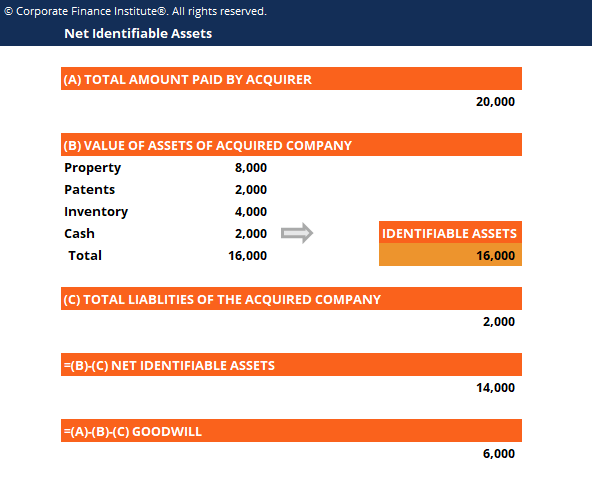

Net Identifiable Assets Template Download Free Excel Template

Fasb 2014 An Appraiser S Guide To Purchase Price Allocation Final

M A Tax Strategy Purchase Price Allocation Winston Street

Valuation Drivers In The Telecommunications Industry Purchase Price Allocation Ppa Methodologies Ernst Yo Contract Agreement Intangible Asset It Network

Corporate Partner Tax Instructor Dwight Drake Asset Sale Old Corp Buyer Old Corp Stockholders Stock Cancelled In Liquidation Business Assets Cash Notes Ppt Download

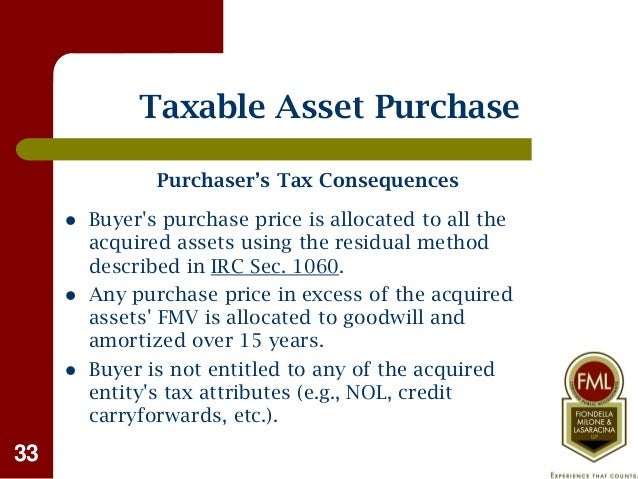

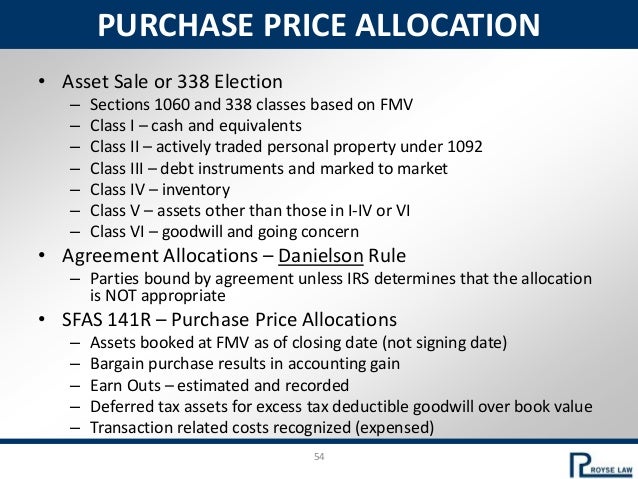

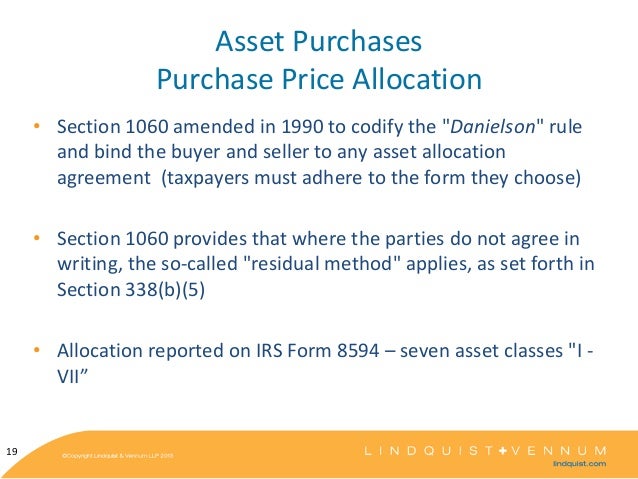

Selling taxpayers sought to disregard allocations made to covenants not to compete and purchasing taxpayers sought to allocate additional amounts to such covenants and away from goodwill.

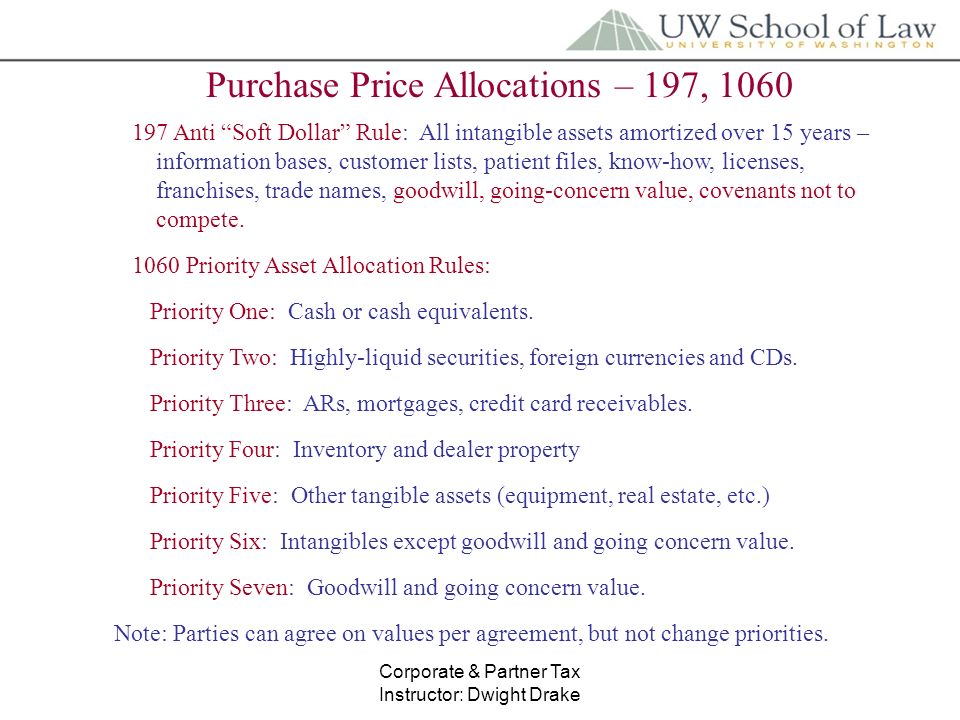

Section 1060 purchase price allocation. 26 cfr 1 1060 1 special allocation rules for certain asset acquisitions. Section 1060 has generally been credited with providing tax certainty for the purchaser and seller where the purchaser and seller agree on an allocation of the purchase price and report the transaction on a consistent basis. Special allocation rules for certain asset acquisitions.

The amendments made by this section enacting this section and renumbering former section 1060 as 1061 shall apply to any acquisition of assets after may 6 1986 unless such acquisition is pursuant to a binding contract which was in effect on may 6 1986 and at all times thereafter. Information about form 8594 asset acquisition statement under section 1060 including recent updates related forms and instructions on how to file. 1 1060 1 special allocation rules for certain asset acquisitions.

Prior to the enactment of section 1060 as part of the 1986 act taxpayers and the government had frequently skirmished over purchase price allocations.

Buying Selling A Business Tax Considerations

Advanced Business Contracts How To Minimize Purchase Price Disputes

M A Tax For 2019

Form8k20160304exh10 1

Corporate Acquisitions Mergers And Divisions Ppt Download

Teifall2013acquisitionagreementfinal Edits V1

Purchase Price Allocation What It Is And Why You Should Get It Right Economics Partners

Broadcom Inc 2019 Current Report 8 K

Kaiser Corp Tax Update 2013

The Challenge Of Purchase Price Allocation

Https Gbq Com Wp Content Uploads 2013 11 Valuation Observations Purchase Price Nov 2013 Pdf

Credit Unions Purchasing Community Banks Winthrop Weinstine

Tax And Corporate Law On Sales And Purchases Of Businesses