Irc Section 170 C

What Is A Letter Of Determination North Texas Giving Day

Tax Exempt Status Letter Of Affirmation By Josh Kufera Issuu

Http Www Bradfordtaxinstitute Com Endnotes Irc Section 170b1a Pdf

The Bizarre World Of Tax Exempt Pedophiles The Post Millennial

2018 Irs Affirmation Letter Pdf Google Drive

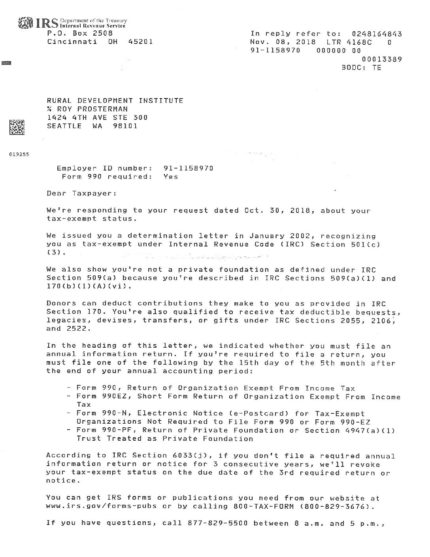

Irs Form 4168 Letter 2018 11 08 Landesa

C charitable contribution defined.

Irc section 170 c. Irc section 170 c 2 a specifically limits the tax deduction to corporations funds or foundations created or organized in the united states or under the laws of the united states. Internal revenue code section 170 f 11 c charitable etc contributions and gifts. Internal revenue code section 170 c 2 charitable etc contributions and gifts.

There shall be allowed as a deduction any charitable contribution as defined in subsection c payment of which is made within the taxable year. A charitable contribution shall be allowable as a deduction only if verified under regulations prescribed by the secretary. 508 d or 4948 c 4 subject to the conditions specified in such sections.

Private shareholder or individual. 170 c 2 a corporation trust or community chest fund or foundation. 170 c 1 a state a possession of the united states or any political subdivision of any of the foregoing or the united states or the district of columbia but only if the contribution or gift is made for exclusively public purposes.

Ii providing for the determination of an amount to be treated as net income of the donee which is properly allocable to qualified intellectual property in the case of a donee who uses such property to further a purpose or function constituting the basis of the donee s exemption under section 501 or in the case of a governmental unit any purpose described in section 170 c and does not possess a right to receive any payment from a third party with respect to such property. No deduction shall be allowed under this section for a contribution to or for the use of an organization or trust described in section 508 d or 4948 c 4 irc sec. For purposes of this section the term charitable contribution means a contribution or gift to or for the use of.

Internal revenue code irc 170.

A Global View Of The Pandemic S Effect On Higher Education

Https Affirmation Org Wp Content Uploads 2019 09 Irs Determination Letters1 Pdf

Gpvcoc Receives Its Official Tax Exempt Certificate From The Irs The Greater Pascack Valley Chamber Of Commerce

Https Www2 Heart Org Site Docserver Updated 2018 501c3 And Umbrella Letter Pdf Docid 4188

Pin On Letter Template

Https Tax Fo Uiowa Edu Sites Tax Fo Uiowa Edu Files Tax 20exemption 20explanation Pdf

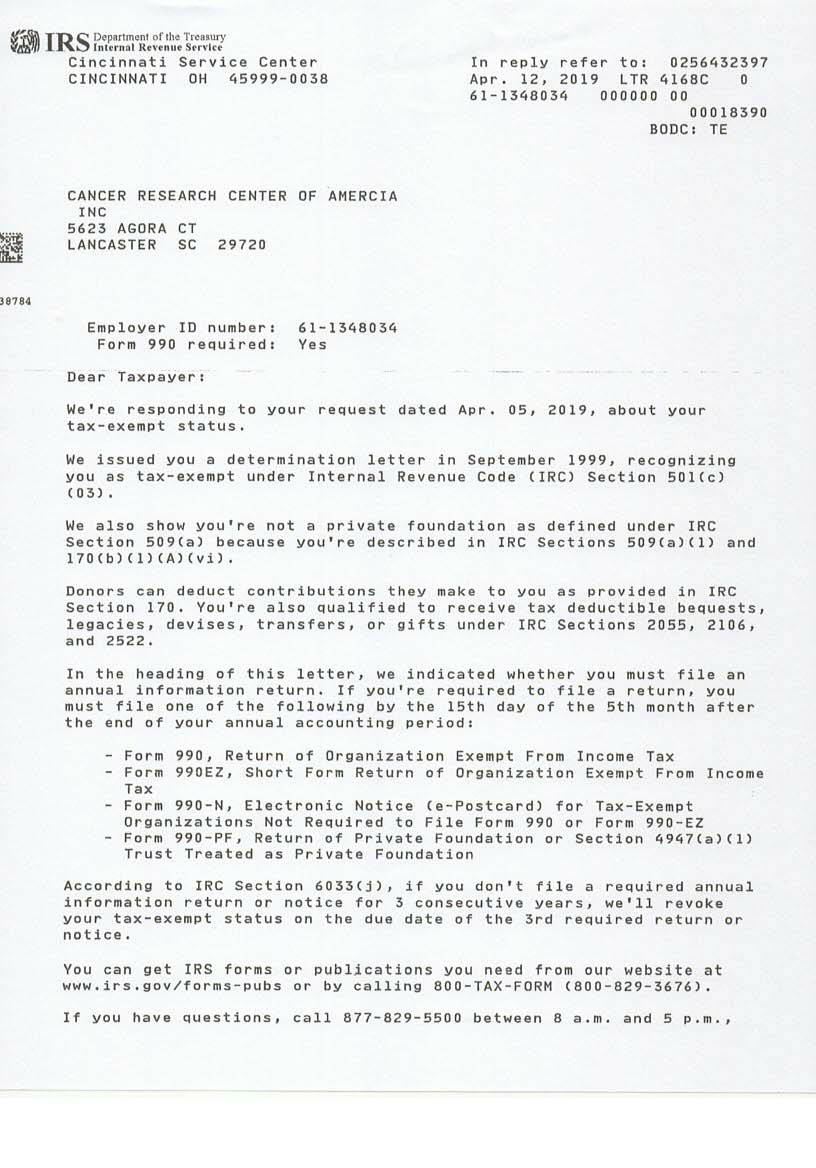

Irs Letters Cancer Research Center Of America Inc

Pantone 170 C Couleur Pantone Pantone Nuancier

Https Bsbproduction S3 Amazonaws Com Portals 29528 Docs Fieldfoundationcapitalcampaign Pdf

Frequently Asked Questions About Tax Exempt Organizations Everycrsreport Com

Google Nonprofit Program Dave Hamby Goes Walkabout Google Apps Non Profit Lettering

Characteristics Of And Reporting Requirements For Selected Tax Exempt Organizations Everycrsreport Com

Cs Remastered