Irc Section 1250

Http Media Straffordpub Com Products Calculating Depreciation Recapture Under Irc 1245 And 1250 Minimizing Tax Through Transaction Planning 2017 08 15 Presentation Pdf

:max_bytes(150000):strip_icc()/GettyImages-1174783581-020e7504020947dc979f864f2ebee096.jpg)

Section 1250 Definition

Irc Section 1250 B 3 Wilson Rogers Company

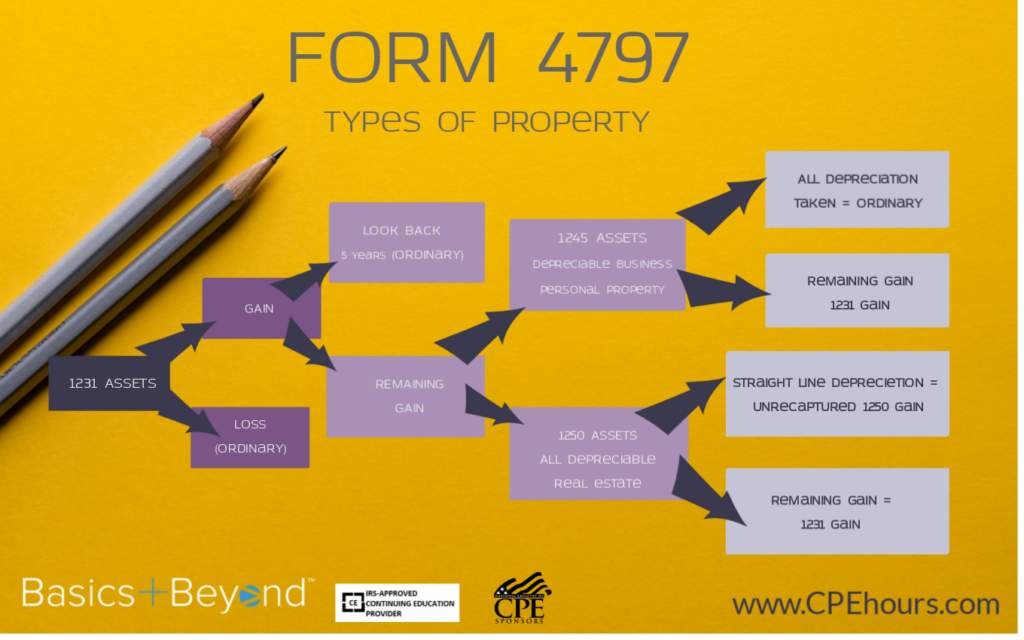

Sale Of Business Assets What You Need To Know About Form 4797 Basics Beyond

1231 1245 And 1250 Property Used In A Trade Or Business

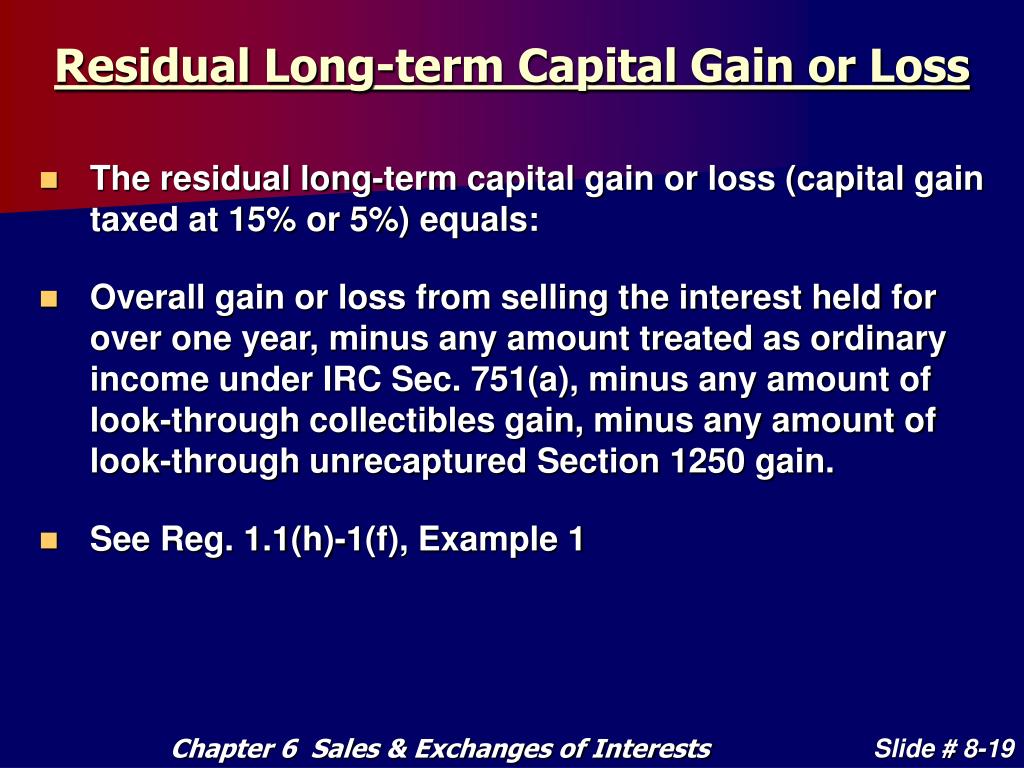

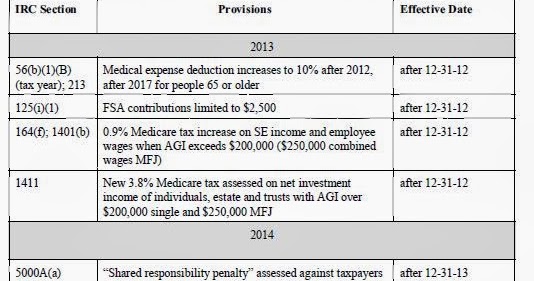

Business Issues Chapter 6 Pp National Income Tax Workbook Ppt Download

31 2017 see section 14202 c of pub.

Irc section 1250. Section 1250 property defined. Retired or demolished property. See example 3 i of paragraph c 4 of 1 1250 3 2 meaning of terms.

In the case of section 1250 property with respect to which a mortgage is insured under section 221 d 3 or 236 of the national housing act or housing financed or assisted by direct loan or tax abatement under similar provisions of state or local laws and with respect to which the owner is subject to the restrictions described in section 1039 b 1 b as in effect on the day before the date of the enactment of the revenue reconciliation act of 1990 100 percent minus 1 percentage point. Depreciation allowed or allowable. Learn about 1231 1245 1250 property and its treatment for gains and losses.

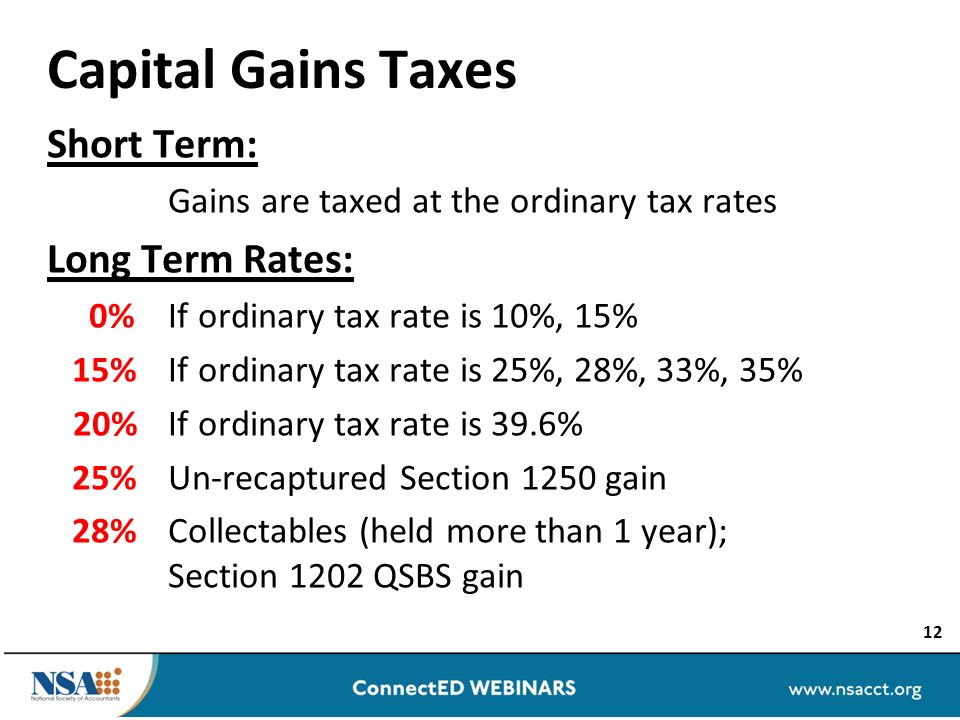

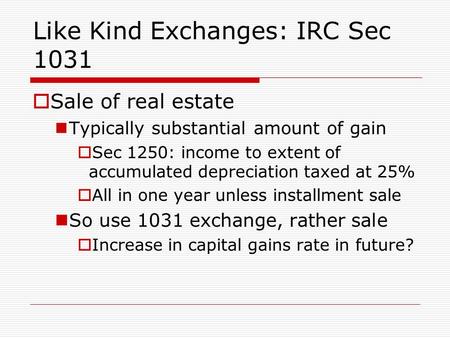

Unrecaptured section 1250 gain is an irs tax provision where depreciation is recaptured when a gain is realized on the sale of depreciable real estate. The internal revenue code includes multiple classifications for property. Depreciation taken by other taxpayers or on other property.

Figuring straight line depreciation. 1 so in original. Property held by lessee.

115 97 set out as an effective date of 2017 amendment note under section 172 of this title. Internal revenue service code states the irs should treat a gain from the sale of depreciated real property as ordinary income. In the case of section 1250 property with respect to which a mortgage is insured under section 221 d 3 or 236 of the national housing act or housing financed or assisted by direct loan or tax abatement under similar provisions of state or local laws and with respect to which the owner is subject to the restrictions described in section 1039 b 1 b as in effect on the day before the date of the enactment of the revenue reconciliation act of 1990 100 percent minus 1 percentage point.

I for purposes of section 1250 the term.

Concepts In Federal Taxation Chapter 11 Property Dispositions Ppt Video Online Download

Https Farmoffice Osu Edu Sites Aglaw Files Site Library Taxpdf Ch 203 20form 204797 281 29 Pdf

Acquisitions Of Subsidiaries Of Freestanding Companies Ppt Download

Https Www Dtcc Com Globals Pdfs 2009 March 04 4573 09

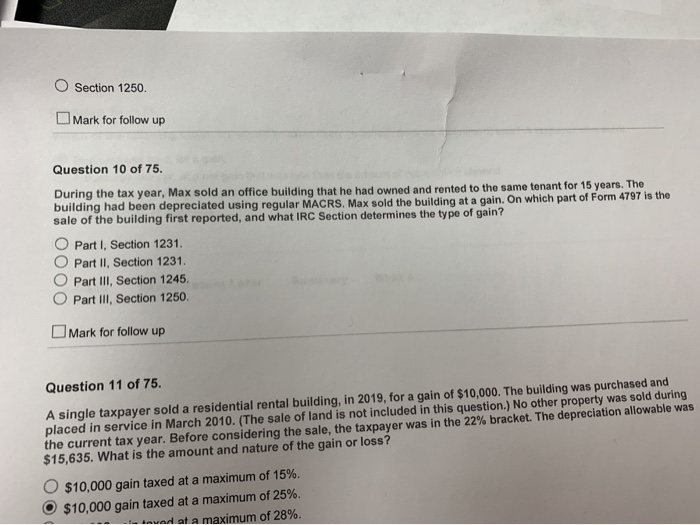

Solved O Section 1250 Mark For Follow Up Question 10 Of 7 Chegg Com

Evaluating Fixed Asset Management Software

Ppt Sales And Exchanges Of Partnership Interests Powerpoint Presentation Id 4110851

The Cpa Journal

3 22 15 Foreign Partnership Withholding Internal Revenue Service

Moores Rowland Tax Consultants

Mc Graw Hill Depreciation Methods Chapter Ppt Download

Http Www Ustaxfs Com Wp Content Uploads 2015 08 Ll Passthrough Supplemental Pdf K1s Pdf

Https Mazarsledger Com Wp Content Uploads 2018 12 Mazars Usa Ledger Nov Dec 2018 Pdf