Internal Revenue Code Section 62

Complete Internal Revenue Code Winter 2021 Edition Law Firms Tax Thomson Reuters

Internal Revenue Code Tax Law Research Federal And Ohio Libguides At Franklin County Law Library

3 12 10 Revenue Receipts Internal Revenue Service

20 1 5 Return Related Penalties Internal Revenue Service

Internal Revenue Bulletin 2020 29 Internal Revenue Service

3 12 16 Corporate Income Tax Returns Internal Revenue Service

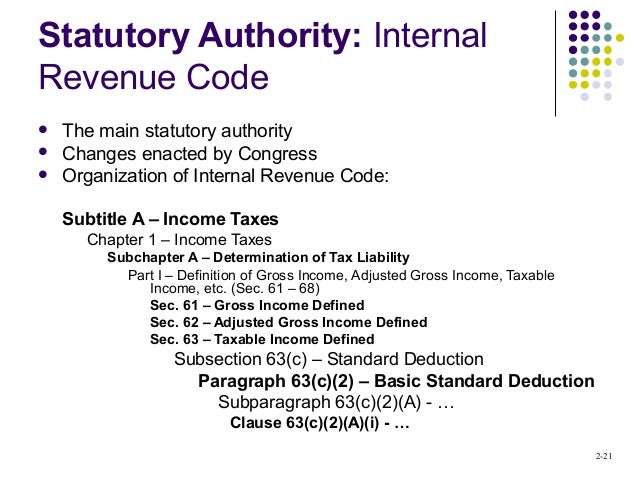

The deductions allowed by this chapter other than by part vii of this subchapter which are attributable to a trade or business carried on by the taxpayer if such trade or business does not consist of the performance of.

Internal revenue code section 62. 95 615 2 nov. 21 attorneys fees relating to awards to whistleblowers any deduction allowable under this chapter for attorney fees and court costs paid by or on behalf of the taxpayer in connection with any award under section 7623 b relating to awards to whistleblowers. 31 1976 and before apr.

For more detailed codes research information including annotations and citations please visit westlaw. 62 a 2 a reimbursed expenses of employees the deductions allowed by part vi section 161 and following which consist of expenses paid or incurred by the taxpayer in connection with the performance by him of services as an employee under a reimbursement or other expense allowance arrangement with his employer. 8 1978 92 stat.

For purposes of this subtitle the term adjusted gross income means in the case of an individual gross income minus the following deductions. Section 62 a 2 a of the code and 1 62 2 b of the income tax regulations provide that for purposes of determining adjusted gross income an employee may deduct certain business expenses paid by the employee in connection with the performance of services as an employee under a reimbursement or other expense allowance arrangement with his employer. Internal revenue code section 62 a 20 adjusted gross income defined.

3097 provided that with respect to transportation costs paid or incurred after dec. 1 trade and business deductions. Subsection a of section 62 relating to general rule defining adjusted gross income is amended by inserting after paragraph 20 the following new paragraph.

3 12 37 Imf General Instructions Internal Revenue Service

25 6 1 Statute Of Limitations Processes And Procedures Internal Revenue Service

Section 1411 Net Investment Income Tax Income Tax Investing Income

Instructions For Form 5471 02 2020 Internal Revenue Service

What Is The 2018 Form 1040 Tax Forms Form Example Tax

How To File A Tax Extension From Iphone Ipad Or Computer Form 4868 With Images Tax Extension Irs Forms Tax Forms

Pin On Template

Affidavit Of Truth The Real Document U S State United States Constitution With Images Truth Contract Law Territories Of The United States

U S C Title 26 The Internal Revenue Code The Unit Court Decisions Kindle

Account Transactions Artisans Bank Accounting How To Apply Cancelled Check

3 11 3 Individual Income Tax Returns Internal Revenue Service

Instructions For Form 1040 Nr 2019 Internal Revenue Service

Pin By Luzzi Gibbs On Arkansas Taxes Business Tax Deductions Internal Revenue Service Tax Deductions